- Skip to main content

- Skip to "About this site"

Language selection

- Français fr

Public Services and Procurement Canada Internal services: Planned results—2021 to 2022 Departmental Plan

Document navigation for "2021 to 2022 departmental plan".

- Previous page

- Table of contents

Internal services are those groups of related activities and resources that the federal government considers to be services in support of programs and/or required to meet corporate obligations of an organization. Internal services refers to the activities and resources of the 10 distinct services that support program delivery in the organization, regardless of the internal services delivery model in a department. These services are:

- management and oversight services

- communications services

- legal services

- human resources management services

- financial management services

- information management services

- information technology services

- real property management services

- materiel management services

- acquisition management services

Planning highlights

To better align resources to meet departmental priorities, Public Services and Procurement Canada (PSPC) will continue embedding integrated business planning across the department through the implementation of its evergreen integrated business plan, which it launched for the first time in May 2020. At the same time, the department will ensure information regarding its activities and results is more effectively communicated to Parliament and Canadians.

PSPC continues efforts to ensure compliance with proactive publication requirements under the Access to Information Act . To further support the government's commitment to openness and transparency, PSPC is developing a departmental transparency strategy to provide Canadians with relevant and timely information related to the department's mandate. As part of this approach, PSPC has published detailed information online about COVID-19 contracts.

The department is continuing to modernize the way it engages with Canadians and its employees by enhancing proactive communications approaches and its use of social media platforms to better reach its varied audiences. In 2021, management of PSPC web content will be centralized, allowing better integration of messages and supporting a user-centric, accessible and task-based approach to the provision of information and services. Communication approaches will be informed by the diverse information needs of PSPC employees, clients and partners, and the public, and aligned with the department's Integrated Business Plan and support the Minister's mandate and priorities.

Given PSPC 's role as common service provider, the department has a unique opportunity to be a leader and support its clients in reconciliation efforts. Important action is underway across the department, however, an overarching strategy is needed to ensure a coordinated approach across the organization and with Indigenous partners. To meet this need, the Reconciliation and Indigenous Engagement Unit is developing a Reconciliation Strategy to support all PSPC reconciliation and Indigenous engagement activities and identify opportunities to develop and enhance policies, programs and initiatives that will advance reconciliation.

With respect to diversity and inclusion, PSPC will continue the dialogue it initiated in 2020 to 2021 with diverse groups of employees on their lived experience at the department. This dialogue will allow the department to frame and refine its actions related to shifting departmental culture; improving the recruitment, development and promotion practices; and addressing barriers in the delivery of programs and services. The department's executives and middle management will continue their learning path on unconscious bias and anti-racism, with a view to engaging all PSPC employees on this important topic. PSPC will continue to develop targeted recruitment and development strategies and provide services, tools, and expert advice to hiring managers to promote a more inclusive workplace and to ensure the department's workforce reflects the diversity of Canada's evolving population.

In support of mental health, PSPC will continue to provide mental health tools for managers and employees, virtual access to all mental health and well-being services and mental health ombudsman's individual consultations, as well as increase mental health visibility and awareness.

PSPC is looking to optimize security throughout the department by continuing to deliver on a 3-year Departmental Security Plan and building security specialist capacity and expertise across the department. This will be accomplished through program transformation initiatives or leading innovative projects taking into account the evolving security landscape.

In support of its implementation of the Treasury Board Secretariat Policy on Service and Digital , PSPC will continue engaging with the service providers within PSPC branches to establish service management, service delivery practices, communities of practice, governance as well as systems that will enable the department to access its "one PSPC " vision in a predominantly digital and cloud ready landscape.

There are a number of risks that could impact the successful delivery of internal services.

Data analytics

There is a risk that PSPC will not be able to readily access reliable data and will not have the expertise needed to analyze it in order to make timely and informed decisions. To mitigate this risk, PSPC will implement the required data repositories like data warehouses, and will continue to invest in other data analytics capacity tools and related strategies. In addition, PSPC 's digital services will implement its recently-developed Human Resources Strategy, which will focus on developing capacities within data analytics, data science and artificial intelligence.

Departmental coordination

There is a risk that the diversity of PSPC 's varied business lines will impact the department's ability to collectively plan, and to make resourcing decisions that will achieve departmental results and support a culture of "One PSPC ". To mitigate this risk, PSPC will continue strengthening its department-wide integrated planning process, which includes the integrated business plan. This will improve PSPC 's common approaches to strategic and operational planning, budgeting, resource allocation, and performance monitoring and reporting. PSPC will also take advantage of opportunities for increased collaboration by strengthening its strategic policy function, promoting and reinforcing the "One PSPC " approach in planning and communication, and continuing to adapt training and governance structures. This will ensure a better alignment of resources with core priorities and more consistency in client service experiences.

Departmental risk management culture

There is a risk that PSPC 's departmental risk management culture change initiative will not foster the adaptability needed to seize opportunities and minimize threats in an integrated manner, while also maintaining the resilience required to safeguard trust in its ongoing ability to deliver. To mitigate this risk, PSPC has undertaken a number of important initiatives. These include developing a coherent and strong risk management framework, regularly renewing the department's risk profile in order to communicate key strategic risks, and developing a new risk tolerance approach, which will be progressively implemented across PSPC through stakeholder and partner engagement on pilot projects.

PSPC will continue building collaborative relationships between its integrated risk management and integrated business planning units, as well as business line specialists, in order to capture and communicate opportunities and threats to the department's operational priorities, as well as in managing risks linked to shared accountabilities with other departments.

Digital transformation

There is a risk that PSPC will not continue to have the modern and reliable systems, expertise and cyber safeguards needed to effectively operate and deliver services in a predominantly digital environment, which now includes a much increased full-time and department-wide reliance on telework. To mitigate this risk, the department has implemented new virtual team environments and collaborative tools, including Teams and other Microsoft 365 applications. PSPC also created the Cloud Competency Centre, and is currently engaging with the private sector in order to establish delivery systems that will enable the department to acquire the in-house expertise needed to improve cloud readiness. PSPC will also implement the recently developed Digital Services Human Resources Strategy, the information technology (IT) Project Management Framework, and a cybersecurity management action plan to adapt to the changing digital environment.

Recruitment and retention

There is a risk that PSPC will not be able to attract and retain the specialized, skilled and diverse workforce needed to deliver timely and quality services to its clients. To mitigate this risk, PSPC has implemented a cohesive, department-wide People Management Plan that is aligned with the department's integrated planning processes. This plan is helping to prioritize human resources programs and strategies, and to integrate leadership development and succession planning. Maintaining and refreshing the People Management Plan, as well as continuing the implementation of other staffing and talent management modernization initiatives, will enable PSPC to attract and retain the specialized and diverse staff required to deliver on its plans and priorities. These initiatives, along with ongoing efforts by the Office of the Mental Health Ombudsman as well as regular check-ins with staff, seek to mitigate impacts of a work environment currently experiencing rapid and frequent changes. PSPC continues to take steps to address challenges around workload management and promote work/life balance.

Planned budgetary financial resources for internal services

The decrease in net planned spending is mainly due to the completion of information technology projects and a decrease in spending for some projects in subsequent years such as the Government of Canada trusted platform project and the digital convergence project. The net decrease is also due to the end of incremental funding for human resources services to employees for the pay administration initiative. Funding will be adjusted should future approvals be received.

Financial, human resources and performance information for Public Services and Procurement Canada's program inventory is available in the Government of Canada InfoBase .

Planned human resources for internal services

Language selection

Introduction to integrated business and human resources planning (cor121), available offerings.

To register, you will be prompted to sign in.

Sign in to register

Delivery method

Description.

Integrated business and human resources planning enables the management of talent that organizations need to successfully deliver programs and services to Canadians. This online self-paced course presents the principles and concepts behind integrated business and human resources planning (IBHRP) in the federal public service. Participants will learn about the benefits of human resources planning, key considerations for integrated planning, and workforce management strategies that can help achieve business objectives.

Topics include:

- defining IBHRP

- identifying common challenges of IBHRP

- reviewing the legal accountabilities, roles and responsibilities of key players

- managing talent through workforce management strategies

- reviewing the legislative framework

Legacy course code: H300

Mobile App: Reconciliation: A Starting Point

Download the "Reconciliation: A Starting Point" app to access a wealth of information on Indigenous Peoples in Canada, key historical events, and reconciliation.

Indigenous Learning Series

Discover Canada's shared history with First Nations, Inuit and Métis Peoples.

Have something to share?

We want to hear from you!

The School is committed to client service excellence and welcomes your comments. Your feedback helps us understand your learning needs and improve the delivery of our programs and services.

Share your feedback , suggestions, compliments or complaints.

General inquiries

Contact the School's Client Contact Centre for help with registration, technical issues or other questions.

Integrated Business Planning

Today’s market requires businesses to plan more rapidly and assess multiple scenarios at once. We help connect leading technologies and bespoke methodologies through integrated business planning to break down silos and unlock new routes to savings and growth.

Mike Ballestrin

EY Canada Finance Consulting Leader

KB Brinkley

EY Canada Integrated Business Planning Leader

What EY can do for you

Business, markets, expectations and technology have all changed. These monumental shifts necessitate a new framework for business planning, one that’s more integrated than ever before.

Integrated business planning is about connecting what finance and the business are doing, so the organization can react more quickly to any number of external changes, shocks or disruptions. That collaborative approach accelerates speed to impact.

We’ve created a distinctive, integrated approach to business planning that can set your organization apart. Our approach is scalable to meet the specific needs of any given business, at any stage on the growth journey. We work with organizations to build a customized integrated business planning framework that:

- Dismantles operational silos and aligns processes so functional groups can make better decisions around strategic direction and tactical execution

- Employs machine learning, AI and proprietary EY accelerators to deliver up-to-date insight

- Empowers clients to better understand the state of play

- Surfaces insight to help decision-makers buy, invest, manage and save

- Creates a sustainable, transparent and controlled method of planning ahead

- Cultivates shared planning ownership between finance and operations

- Leverages world-class strategic alliances to help organizations abandon outdated, manual ways of working and embrace new possibilities

Our IBP services include:

- Full-service process and technology implementation

- Upfront collaboration session to define and align key business objectives with stakeholders across functions

- EY wavespace session to co-create an action plan and build out the future vision for your organization on IBP

- Rapid assessment to baseline performance, applying advanced EY tools and building transformation business cases

- Prioritization and implementation of use cases to realize benefits of IBP

Applying integrated business planning is key to navigating market complexity and long-term financial health. The best-performing companies merge operational and financial planning to foster agility and drive valuable bottom-line results. By bringing together better tech, better thinking and better cross-functional teaming, we can tailor our approach to your specific industry or business journey. This is how we empower clients to overcome today’s challenges, drive material improvements to financial performance, scale up and set ambitious new organizational and growth goals.

EY alliance and ecosystem relationships for integrated business planning

Our roster of key alliances and partnerships enables accelerated transformations tailored to the most specific industry and business journeys.

Our latest thinking

Like what you’ve seen? Get in touch to learn more.

Connect with us

Our locations

Legal and privacy

Accessibility

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

EY | Assurance | Consulting | Strategy and Transactions | Tax

EY is a global leader in assurance, consulting, strategy and transactions, and tax services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© EYGM Limited. All Rights Reserved.

EYG/OC/FEA no.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

Welcome to EY.com

In addition to cookies that are strictly necessary to operate this website, we use the following types of cookies to improve your experience and our services: Functional cookies to enhance your experience (e.g. remember settings), and Performance cookies to measure the website's performance and improve your experience . , and Marketing/Targeting cookies , which are set by third parties, allow us to execute marketing campaigns, manage our relationship with you, build a profile of your interests and provide you with content or service offerings in accordance with your preferences.

We have detected that Do Not Track/Global Privacy Control is enabled in your browser; as a result, Marketing/Targeting cookies , which are set by third parties that allow us to execute marketing campaigns, manage our relationship with you, build a profile of your interests and provide you with content or service offerings in accordance with your preferences are automatically disabled.

You may withdraw your consent to cookies at any time once you have entered the website through a link in the privacy policy, which you can find at the bottom of each page on the website.

Review our cookie policy for more information.

Customize cookies

I decline optional cookies

Language selection

- Français fr

Audit of the Management of Procurement Services

Presented to the Departmental Audit Committee (DAC) July 11, 2022

Table of Contents

Introduction, areas for improvement, internal audit conclusion and opinion, statement of conformance, audit purpose and objectives, audit considerations, approach and methodology, governance and compliance, procurement processes.

- Human Resource Planning and Training

Transition to the new Directive on the Management of Procurement

Appendix a – audit criteria, executive summary.

The procurement function serves as a mechanism for organizations to acquire the goods and/or services they require to advance organizational needs and priorities. Procurement methods include: sole-source contracting, competitive contracting, supply arrangements and standing offers, purchase orders, and acquisition cards.

Natural Resources Canada (NRCan) is subject to a suite of procurement-related instruments that include legislative, policy, and regulatory instruments, which are managed by the Treasury Board of Canada Secretariat (TBS) and its central purchasing agents, Public Services and Procurement Canada (PSPC) and Shared Services Canada (SSC). These instruments outline the responsibilities for managing and executing procurement activities. Of note is the ongoing departmental transition to a new overarching Treasury Board (TB) policy and associated directives that cover the management of procurement. Fully effective May 13, 2022, the new Policy on the Planning and Management of Investments and the Directive on the Management of Procurement serves as the main procurement related policy suite.

Within NRCan, the Assistant Deputy Minister (ADM) of the Corporate Management and Services Sector (CMSS) is the Senior Designated Official (SDO) with authority and functional responsibility for procurement related activities. The SDO is responsible for supporting the Deputy Minister’s accountability for all requirements detailed within the TB Policy and Directive on the Management of Procurement.

Within CMSS, the Finance and Procurement Branch (FPB) is responsible for the core operations of the procurement function. All managers across all sectors have delegated contracting authority; however, it is restricted. The Lands and Minerals Sector (LMS) through the Surveyor General Branch and the Polar Continental Shelf Program, and the Communications and Portfolio Sector (CPS) hold increased procurement-related delegated authorities for specific purposes, such as procuring land surveys and printing services. While the FPB holds primary responsibility for procurement oversight and activities, all sector business owners are responsible for planning their procurement activities and ensuring that requests are submitted for action.

The objective of this audit was to assess the effectiveness and efficiency of management processes related to the procurement function, and the adequacy of governance over procurement operations, as it relates to meeting the needs of the Department.

Overall, FPB has established oversight mechanisms for procurement activities at the operational level to facilitate compliance with policy requirements, and procurement activities and processes generally comply with government policy requirements. The Department has also made progress in implementing action plans to address the recommendations from the recent Office of the Procurement Ombudsman (OPO) Review. In addition, FPB has made significant efforts to implement the COVID-19 Vaccination Policy for Supplier Personnel, which came into effect in November 2021.

The Department has also designed and implemented processes and procedures in support of procurement activities, and this information is readily available to sectors/business owners. Despite delays in processing, business owners conveyed their overall satisfaction once their procurement requests were actioned.

As part of the transition to the new TBS Directive on the Management of Procurement, the Department has developed a Procurement Management Framework.

There is a need to enhance governance for strategic and integrated procurement planning and to encourage active participation by the sectors. Improvements are needed to better define the roles and responsibilities of the Procurement Policy, Analysis and Reporting Unit (PPAR) and the Procurement Services Unit (PSU), to enhance communication and collaboration.

In addition, changes are required to ensure that procurement-related guidance is regularly reviewed and updated, constraints in the current procurement processes are examined, and service standards are evaluated for relevance and potential data gaps to address any performance challenges. Further, there is a need for FPB to improve and strengthen its communication mechanisms with sectors.

Additional work is required to document FPB’s human resources (HR) and succession planning and monitoring processes; to enhance staff training requirements; and to strengthen processes for knowledge transfer and sharing. These actions would support resourcing needs, enhance the staff training complement, and ensure that potential knowledge disparities between staff members are reduced.

In my opinion, the Department has elements of an effective procurement function and some adequate oversight mechanisms but a number of improvements are required to enhance the efficiency and effectiveness of management processes. Additional opportunities exist to formalize and strengthen HR and succession planning processes, and training initiatives.

In my professional judgement as Chief Audit Executive, the audit conforms with the Institute of Internal Auditors' International Standards for the Professional Practice of Internal Auditing and the Government of Canada’s Policy on Internal Audit, as supported by the results of the Quality Assurance and Improvement Program.

Michel Gould, MBA, CPA, CIA Chief Audit and Evaluation Executive July 11, 2022

Acknowledgements

The audit team would like to thank those individuals who contributed to this project and particularly employees who provided insights and comments as part of this audit.

The procurement function serves as a mechanism for organizations to acquire the goods and/or services they require to advance organizational needs and priorities. Procurement methods include: sole-source contracting, competitive contracting, supply arrangements and standing offers, purchase orders, acquisition cards, and temporary help services.

Within the Government of Canada, procurement activities are governed by a complex series of legislative, policy, and regulatory instruments, managed by the Treasury Board of Canada Secretariat (TBS) and its central purchasing agent, Public Services and Procurement Canada (PSPC). Integral instruments for financial management and procurement activities include: the Financial Administration Act (FAA), Government Contracts Regulations, and the Treasury Board (TB) Contracting Policy. Additional policies and directives support these instruments, such as the TB Policy on Green Procurement, the TB Directive on Government Contracts, including Real Property Leases, in the Nunavut Settlement Area, and requirements defined to ensure that legal obligations are adhered to in modern treaties (Comprehensive Land Claim Agreements) relating to procurement activities. These instruments serve to provide direction, and when in compliance with these instruments, procurement activities would be conducted in a fair and transparent manner, provide value for money, and demonstrate sound stewardship.

Natural Resources Canada (NRCan) is subject to these instruments, including the TB Contracting Policy. Fully effective May 13, 2022, a new overarching policy, the Policy on the Planning and Management of Investments and its associated directives covers the management of procurement, investment planning, real property, and materiel management. This new policy suite and associated directives replace the TB Contracting Policy, and previous policy coverage in the listed areas. They serve as the main procurement related policy suite. Currently, NRCan is in the process of transitioning to the new policy suite and its associated directives, which includes designating a senior official (termed the Senior Designated Official - SDO) to be responsible for supporting the Deputy Minister’s accountability for all requirements under the new Policy, and developing and implementing a departmental Procurement Management Framework (PMF).

NRCan has designated the Assistant Deputy Minister (ADM) of the Corporate Management and Services Sector (CMSS) as the SDO with authority and functional responsibility for procurement related activities. These activities are managed by the Finance and Procurement Branch (FPB) and its functional units, the Procurement Services Unit (PSU) and the Procurement Policy Analysis and Reporting Unit (PPAR). Outside of FPB, the Lands and Minerals Sector (LMS) through the Surveyor General Branch and the Polar Continental Shelf Program, and the Communications and Portfolio Sector (CPS) hold additional procurement related delegated authorities beyond those held by other sectors. These delegated authorities are held for specific purposes, such as procuring land surveys and printing services. While the FPB holds primary responsibility for procurement oversight and activities, all sectors are responsible for planning their procurement activities and ensuring that requests are submitted to PSU for action.

Generally, items below a monetary threshold of $5,000 can be acquired through the use of an acquisition card. As of May 24, 2022, this limit was increased to $10,000. All other procurement requests must be submitted to FPB through the eProcurement contracting system, except for those initiated and managed by sectors with special procurement delegations for specific purposes as stated above. The eProcurement system is a request intake system used by CMSS that interfaces with the AMI system to track and assign requests to procurement officers. NRCan’s delegated authority for procuring goods, services, and construction internally, without the support of PSPC, is $3.75M for services sourced competitively ($200K sole source), $750K for construction sourced competitively ($100K sole source), and for contractual arrangements, $500K for services and $25K for goods. Requests exceeding these thresholds are processed by PSPC unless specific authorities are obtained through a TB Submission.

The Office of the Procurement Ombudsman (OPO), an independent office within PSPC that assesses whether procurement practices support the principles of fairness, openness, and transparency, recently completed an external review of NRCan’s procurement practices as part of its five year review process that includes 20 federal departments. This external review assessed NRCan’s procurement activities and compliance, in particular for areas in evaluation criteria and selection plans, solicitation documents, and evaluation of bids and contract award, for contracts awarded between January 1, 2018 and December 31, 2019. Given this recent review, the audit took into account the review results, including recommendations and actions taken by CMSS, in order to avoid duplicated efforts in these areas.

During the audit’s scope period (January 1, 2020 to March 31, 2022), 13,849 procurement requests were submitted through the eProcurement system; 8,972 requests were completed; 273 requests were in progress; 1,263 requests were recalled by the originator; 188 were not yet assigned; 136 were pending IT review. This totals $218,104,928.18 in completed requests for this period. This excluded contract amendments and task authorizations, which do not normally go through eProcurement.

Table 1 – Procurement Requests

The audit team recognizes that this scope period coincided with the COVID-19 pandemic, which impacted the regular operations of the procurement function. However, this did not impact the ability to carry out the audit within the planned timeframe.

This audit was included in the 2021-2026 Integrated Audit and Evaluation Plan, approved by the Deputy Minister on May 5, 2021.

The objective of the audit was to assess the overall adequacy of governance, management processes and controls supporting the implementation of a department-wide plan to fulfill the Department’s Open Government obligations and further facilitate the delivery of its broader mandate.

Specifically, the audit assessed whether:

- Adequate governance and oversight mechanisms exist to provide strategic and operational guidance, enable the transition to the new policy suite, and facilitate compliance with GOC policies and guidance;

- Effective and efficient business processes and communications mechanisms are in place, and are operating effectively to support NRCan’s procurement needs and activities; and

- Effective resource planning, succession planning, and capacity building processes and mechanisms exist, and that they are operating effectively to support NRCan’s procurement function.

A risk-based approach was used in establishing the objectives, scope, and approach for this audit engagement. A summary of the key underlying potential risks that may impact the effective management of NRCan’s procurement services include:

- Adequate governance structures and efficient business processes to manage the Department’s procurement function and activities in compliance with relevant government policy instruments;

- Effective processes and mechanisms to transition to the new TB policy suite;

- Clearly defined roles, responsibilities, and accountabilities pertaining to procurement processes and activities;

- Effective mechanisms that enable frequent and timely two-way communication between sectors and the procurement function;

- Effective human resource planning, including succession planning, capacity building, and training to ensure that the Department’s procurement activities are well supported; and

- Effective knowledge transfer processes to ensure that pertinent information is retained within the procurement function.

The scope of the audit focused primarily on FPB/CMSS procurement processes and activities in compliance with existing government policy requirements, their capacity to advance departmental procurement priorities and needs, and their ability to support sectors in delivering on their objectives through procurement activities. The audit also included the procurement activities managed by sectors who hold special procurement related delegations. Further, the audit examined FPB’s activities for transitioning to the new Directive on the Management of Procurement.

The audit examined procurement activities from January 1, 2020 to March 31, 2022, in order to include the most recent activities and processes. The audit did not assess or provide an opinion on procurement evaluation results as this was assessed in the OPO external review, and did not include construction contracts or procurement activities that fall outside of the scope of NRCan’s authorities, such as those procured through PSPC or Shared Services Canada (SSC). However, the audit examined the advice provided to sector clients and internal processes that are used for requests sent to PSPC and SSC.

The scope of the audit did not examine acquisition cards and related processes, due to recent and ongoing continuous audit coverage in this area, nor did the audit examine the directives within the new TB policy that do not pertain to procurement.

In addition, the audit considered the methodology and results of recent internal control assessments conducted by the Financial Policy, Reporting and Internal Controls Division within CMSS.

The results of other previous advisory, audit, and evaluation projects on related topics were also considered where deemed relevant in order to inform the audit and reduce duplication of efforts.

The approach and methodology used in this audit followed the Institute of Internal Auditors' International Standards for the Professional Practice of Internal Auditing (IIA Standards) and the TB Policy on Internal Audit. These standards require that the audit be planned and performed in such a way as to obtain reasonable assurance that audit objectives are achieved. The audit included tests considered necessary to provide such assurance. Internal auditors performed the audit with independence and objectivity as defined by the IIA Standards.

The audit approach included the following key tasks:

- Interviews with key FPB personnel and sector representatives;

- A review of selected key documents, business processes, and communication materials;

- File review of a sample of procurement requests and completed files - a judgmental sample of 25 procurement files (10 sole source contracts for goods under $25K and services under $40K, 15 competitive) was reviewed and assessed for appropriate levels of financial signing authority, sufficient documentation on sole source contracts, evidence of solicitation for competitive contracts, completion of security requirements where applicable, and proactive disclosure where applicable; and

- Walkthroughs of key procurement processes, such as the contracting process and the quality assurance process.

The criteria were developed based on key controls set out in the Treasury Board of Canada’s Audit Criteria related to the Management Accountability Framework – A Tool for Internal Auditors, in conjunction with the TBS Directive on Procurement, and relevant associated policies, procedures, and directives. The criteria guided the fieldwork and formed the basis for the overall audit conclusion.

Appendix A summarizes the detailed audit criteria.

The conduct phase of this audit was substantially completed in March 2022.

Please refer to Appendix A for the detailed audit criteria. The criteria guided the audit fieldwork and formed the basis for the overall audit conclusion.

Findings and Recommendations

Summary finding.

Overall, FPB has established oversight for procurement activities at the operational level to facilitate compliance with policy requirements. While governance structures and mechanisms to manage the Department’s procurement activities are in place, they are not adequate to provide strategic and operational guidance, and are not being leveraged or used consistently. There are also opportunities to enhance the annual procurement planning process to ensure that procurement priorities are communicated and utilized to support strategic and integrated procurement planning.

Roles, responsibilities and accountabilities related to the procurement process are clearly defined, documented, and communicated; however, they are not all up-to-date. In addition, PPAR and PSU have an opportunity to better define their internal roles and responsibilities in order to improve communication and collaboration.

Procurement activities and processes generally comply with government procurement policy requirements. In addition, FPB has made progress in implementing action plans to address the recommendations from the recent OPO Review, and is on track to meet most timelines. FPB has also made significant efforts to implement the COVID-19 Vaccination Policy for Supplier Personnel, which came into effect November 2021.

Supporting Observations

Effective governance and oversight mechanisms should be in place to provide strategic direction and to ensure compliance with Government of Canada policies and guidance. The audit examined whether governance structures and mechanisms for procurement activities are clearly defined, provide strategic and operational direction, and provide oversight for the Department’s procurement activities, including compliance with relevant government policy instruments. Further, the audit examined whether roles, responsibilities, and accountabilities related to the procurement process are clearly defined, documented, and communicated to relevant parties.

Governance and Oversight

At the operational level, the primary oversight mechanism over procurement activities is the quality assurance (QA) function conducted by PPAR. Procurement files are reviewed and assessed to ensure compliance with government policy instruments. Deficiencies in the processing of procurement files are identified and efforts are made to correct issues through training and awareness. Files are generally reviewed and assessed after completion; however, there are instances where PPAR conducts QAs prior to tendering to ensure that required elements are included when processing the procurement requests. PPAR also monitors and reports on departmental procurement activities; this includes mandatory reporting such as on procurement activities related to Comprehensive Land Claim Agreements and other modern treaties to Indigenous Services Canada, and discretionary reporting.

There is currently no designated governance committee being used for strategic procurement planning. Previously, the ADM-level Procurement Review Board (PRB) served as the governance body for reviewing and providing recommendations or direction on complex and high risk procurement activities, with the ADM CMSS/ Chief Financial Officer (CFO) making the final decisions. As the number of decisions being brought to PRB declined, and as the committee was mainly being used for secretarial approval of procurement activities, it was dissolved in 2020.

The ADM-level Departmental Operations Committee (DOC) was identified as the appropriate forum for the ADM CMSS/CFO to bring forward procurement issues for discussion as needed, at their discretion. Since the DOC’s inception in April 2021, there have been no specific discussions on procurement issues. The audit team noted that procurement issues have been discussed at the DG-level Finance and Real Property Committee (FRPC). This includes an update on procurement, such as completed, ongoing, and planned actions for addressing the high volume of unassigned requests and workload. Procurement issues are also discussed as part of CMSS’ sector management committee meetings, and at a recent Senior Management Committee meeting held in early 2022. These efforts provide a degree of oversight over procurement activities; however, they are not sufficient to provide strategic direction for the function.

Strategic Procurement Planning

FPB leads an annual procurement planning exercise in consultation with most of the sectors. Requests for information (call-outs) and a procurement planning template are sent to Directors General at the beginning of the fiscal year to solicit information about anticipated complex procurement requirements. The template contains information on required procurement, anticipated contracts with former public servants, and information on anticipated procurement in the Nunavut Settlement Area. This information is intended to enable the PSU to plan, prioritize, and manage their requests by ensuring capacity, managing workload, and optimizing bulk purchases or standing offers for efficiencies, and to support PPAR with their various reporting requirements. Guidance information on the planning exercise is provided to employees on the departmental intranet, The Source.

Although there is a documented procurement planning process, the exercise has not been leveraged or used consistently, and procurement planning information is not effectively solicited/or received from sectors. FPB indicated that many sectors do not respond to the request for procurement requirements, and those that are returned to FPB often do not contain a complete list of planned procurement requirements. Ideally, these plans would allow PSU to inform sectors’ needs and priorities into their own activities and allow them to assess internal capacity requirements. Without a collaborative approach and sector participation to gather information for procurement planning, this may limit procurement planning at the strategic level, and procurement prioritization at the operational level.

Sectors indicated that procurement planning happens at the working level within sectors and is not well integrated with other planning functions in the Department. Over the past year, FPB has made efforts to meet with sectors to acknowledge and to address the backlog of procurement requests by holding engagement sessions at sectors’ management committee meetings. These discussions include prioritization of unassigned requests, the state of procurement, and a broader discussion about the results of the Department’s integrated business planning exercise.

As per the TB Policy on the Management and Planning of Investments, departments are required to ensure that departmental investment planning is integrated with other functions, including procurement, real property, and materiel management. NRCan has been making progress towards developing an investment plan management framework that includes procurement considerations and alignment with department's integrated business planning activities. These actions are in response to the findings and recommendations from the recent Audit of Strategic and Operational Planning Process (2019) and the internal controls assessment on investment planning (2020). As part of implementation of the framework, the Department will be initiating a pilot approach to investment planning, which includes an enhanced and more integrated procurement planning exercise.

Roles and Responsibilities

The key participants in the procurement process are the sectors/business owners and the contracting authorities. A business owner (or sector client who uses FPB’s procurement services) is an individual who is responsible for the business or program area for which the project, procurement, or program is established. A contracting authority is a person who has delegated contracting authority to enter into a contract or contractual arrangement on behalf of a department or agency. The procurement officers within the PSU are all contracting authorities. Programs with special delegations for procurement are also contracting authorities. PPAR provides policy guidance on the operations of the procurement function.

Roles, responsibilities, and accountabilities related to the procurement process are clearly defined documented and communicated to relevant parties via the departmental intranet, The Source. However, this information has not been updated since 2020, with some documents last updated in 2015 and 2018. Business owners interviewed during the course of the audit indicated that they are aware of their roles, responsibilities, and accountabilities relating to procurement, but they expressed a need to be informed of any relevant changes.

Within the procurement function, PPAR and PSU have an opportunity to better define expectations of their internal roles and responsibilities in order to improve communication and collaboration, especially with the changes to procurement procedures resulting from the implementation of the new Directive. This includes a disparity in expectations regarding updating and maintaining procedural and guidance documents (e.g., desktop procedures), and for engagement with business owners on changing procedures.

Procurement activities and processes tested as part of the audit generally comply with government procurement policy requirements. Specifically, testing included: verification of a valid Section 32 approval; security requirements checklists on file; Contract Planning and/or Advance Approval (CPAA) on file; verification of sole source justifications (where applicable); and proactive disclosure requirements. This testing did not duplicate the efforts of the OPO external review, which focused on procurement activities and compliance with government policy requirements, in particular for areas in evaluation criteria and selection plans, solicitation documents, evaluation of bids, and contract award. In addition, the oversight provided by PPAR, through the QA review function and the monitoring and reporting of procurement activities helped facilitate compliance. There were no significant deficiencies or noncompliance identified in the sample files reviewed for the audit.

FPB has established an internal working group and distributed tasks to procurement officers for implementing action plans in response to the eight recommendations from the recent OPO external review. At the end of March 2022, two recommendations regarding clarity on Indigenous requirements and updating Desktop Procedures were self-assessed by FPB as complete and the other six were in various stages of implementation. The outstanding recommendations include:

- establishing a quality control process to ensure mandatory criteria for bids are defined and communicated;

- updating internal guidance for the development of bid evaluation criteria and bid selection methodologies;

- establishing a process for and documenting communication to suppliers for prior to bid closing, for contract aware notices, and for sending regret letters;

- establishing processes to ensure consistent instructions for bid evaluators; non-compliant bids are disqualified and not further assessed; and technical evaluations adhere strictly to the evaluation criteria and scoring grids in solicitations;

- establishing processes to ensure bid evaluations and procurement files are appropriately documented; and

- establishing a process to review planned procurements to ensure aggregate requirements are not inappropriately divided to circumvent controls and / or existing agreements.

The implementation of all action plans related to the OPO Review, such as updating internal guidance for the development of evaluation criteria, establishing processes to ensure that evaluations are appropriately documented, and updating Contracting Desktop Procedures, will allow FPB to continually assess its operations and maintain updated documentation for compliance and alignment with government policy instruments. FPB has indicated that they are on track to meet most implementation timelines.

In November 2021, the COVID-19 Vaccination Policy for Supplier Personnel (the Vaccination Policy) came into effect. Under this policy, departments are required to ensure that solicitation and contracts for new procurement requirements include appropriate clauses regarding vaccination certification; that solicitation documents for active procurements (not yet closed) be amended to include the clauses related to vaccination certification; and that suppliers of existing contracts within the scope of the Vaccination Policy be issued letters regarding the new requirements. Guidance from TBS and PSPC continually changed as departments were responding to these requirements. NRCan’s FPB took immediate steps to address the Vaccination Policy by communicating the requirements and implications to business owners and contracting authorities on how to apply the policy; revising and updating existing templates for bid solicitation; notifying suppliers from existing contracts to obtain signed certification if applicable; and verifying and tracking bidder responses in a central repository for monitoring and reporting purposes. FPB has, therefore, made significant efforts to implement the Vaccination Policy, in light of short timelines and changing requirements. This was done while managing existing operational requirements for procurement and while preparing for the transition to the new Directive on the Management of Procurement.

Risk and Impact

In the absence of a clearly defined governance mechanism for procurement, a collaborative approach and sector participation to gather sector information for procurement planning, departmental procurement activities may not be integrated and aligned with overall sector and departmental objectives and strategies.

A lack of clarity on roles and responsibilities within FPB for updating information, guidance, and templates, and for engagement with business owners may result in inaccurate and/or outdated information being utilized by procurement staff throughout the process, and business owners not receiving the support and guidance they require.

Recommendation

Recommendation 1: It is recommended that the ADM of CMSS:

- Define and implement a governance mechanism for strategic procurement planning, including leveraging the pre-existing committees for oversight and direction;

- Establish a mechanism to solicit sector input to enhance strategic and integrated procurement planning; and

- Define and clarify roles and responsibilities between FPB’s PPAR and PSU.

Management Response and Action Plan

Management agrees with Recommendation #1 .

A: The NRCan Procurement Management Framework (PMF) will identify the existing Finance and Real Property Committee (FRPC) as the primary governance body that can provide strategic oversight and direction; as well as the Departmental Operations Committee (OC) where FRPC or the Senior Designated Officer (CMSS ADM/Chief Financial Officer) may present high-risk procurements, as needed, for consideration. The PMF and FRPC Terms of Reference will be presented to FRPC and the SDO for endorsement by September 2022.

Position responsible : Senior Director, Finance and Procurement Services

Timing: September 2022 for the NRCan PMF to be completed and the FRPC Terms of Reference updated and endorsed.

B: In June 2022, FPB launched a new comprehensive Annual Procurement Plan exercise, including soliciting and considering sector input, that both supports how the Department plans and manages investments while reflecting a strategic approach to departmental procurements. It is part of the implementation of the TBS Directive on the Management of Procurement and is also consistent with the messages shared during the Integrated Business Plan (IBP) exercise that information gathered would be broadened to enhance planning. Procurement Planning processes for FY 22/23 are aligned with Financial Situation Reports (FSRs) and will continue to be aligned with the FSR exercise going forward. In preparation for the next IBP cycle (FY 23/24), FPB will work collaboratively with the Planning and Operations Branch, leverage the same tool and advance planning further.

Timing : Completed June 2022. The mechanism to solicit sector input to enhance strategic and integrated procurement planning (i.e., Annual Procurement Plan) was developed and launched on June 8, 2022. The process is ongoing and aligns with FSRs.

C: The NRCan PMF will outline the roles and responsibilities between PPAR and PSU as well as those of Business Owners.

Timing : September 2022 for the NRCan PMF to be completed and endorsed.

Overall, documented processes and procedures have been established in support of procurement activities; however, certain elements are not working efficiently or effectively to support the timely execution of activities, resulting in significant delays within the process that impact business owners’ ability to meet their needs and attain their objectives.

In addition, opportunities exist to ensure that guidance (including procedural documentation, flowcharts, and templates in support of procurement activities) is regularly reviewed and updated to ensure that business owners are leveraging the most current materials in support of their activities. There is also an opportunity to evaluate service standards for relevance, address potential gaps in the data collected, and leverage this information to address performance challenges.

FPB has established mechanisms and processes in order to communicate with business owners; however, there is an opportunity for FPB to improve and strengthen its communication mechanisms and to provide business owners with more consistent and timely communications.

Efficient and effective business processes should be in place to support the management of procurement needs and activities. The audit examined whether planning, prioritization, and communication processes and mechanisms existed, and whether these were being effectively utilized to address and manage business owners’ procurement needs and activities. Further, the audit examined whether processes existed to address procurement requests and conduct procurement related activities to support business owners in delivering on their objectives.

Documentation of Procurement Processes

FPB has defined and documented both internal procurement procedures to be utilized by staff members, and external processes to be leveraged by all business owners with procurement needs. Internal procedures include the PSU desktop procedures, the PPAR reporting standards, QA procedures, and a QA template tool. Internal procedures are sufficient and enable FPB staff to effectively execute their procurement-related responsibilities.

External procurement processes are in place for planning, purchasing goods and services with CMSS’ support, and contract amendments. Further, FPB has developed templates in support of processes, and visual process flowcharts depicting business owner and other party involvement, such as IT, vendors etc. Information available on the departmental intranet, The Source, provides guidance and expected service standards for processing requests to business owners to support them with their procurement needs and activities, and adequately highlights their roles and responsibilities throughout the process. This information is communicated to all sectors via The Source, however, this information is not regularly reviewed or updated to ensure its continued accuracy and relevance. In some instances, FPB has provided guidance to sectors with special delegations, however, there is no specific and updated guidance readily available on The Source or through other information sharing forums.

Procurement Planning and Prioritization

During the audit scope period, the procurement planning process was not regularly conducted or operating as intended, and was subsequently impacting PSU’s ability to adequately plan, prioritize, and manage procurement related needs and activities. This has resulted in procedural ‘bottlenecks’ that are occurring before procurement tickets are assigned to officers for processing. Further, it was indicated by PSU that the information yielded from this exercise is not adequate to allow for the effective management of procurement requests and planning of resourcing needs. As a result, the eProcurement system is the primary mechanism leveraged by FPB to plan, manage, and manually assign tickets to staff. Ticket assignment is based on a first in, first out process, the complexity of the ticket, and staff availability. Staff further prioritize their requests based on workload and ticket urgency. In light of the increased procurement request volume and internal FPB capacity issues, FPB engaged with senior management to proactively prioritize their procurement needs, including needs relating to new programming.

FPB does not regularly solicit the procurement plans and priorities from business owners, apart from the annual planning exercise with limited sector participation. Most business owners interviewed for the audit indicated that the planning process does not meet their needs. Some business owners indicated that they are proactive in sharing their needs with PSU. In the absence of effective planning processes, some business owners will attempt to bypass the system used by PSU in order to escalate the priority of their requests, through direct inquiries to PSU management. This is not a sustainable model, as it ultimately impacts and causes further delays in the processing time for other sector requests.

PPAR is seeking to implement additional planning-related enhancements, such as holding quarterly meetings with business owners to reconfirm their priorities and to set procurement expectations that are feasible. Implementation timelines for this initiative have not yet been established.

Procurement Processes for Requests and Activities

The procurement process involves sectors submitting their procurement needs to PSU via the eProcurement system. PSU will then review requests, seek additional information and documentation, and assign requests to procurement officers for processing. The end result includes a contract awarded for the delivery of services or goods being procured. Although there are sector procurement advisors assigned to provide support, business owners indicated that their need for guidance and direction are not always met. Prior to request submission, the advisors act as a point of contact between business owners and the procurement function, and help answer general procurement questions. The advisors are not regularly involved or invited to sector procurement planning discussions.

Although the established process is being followed, based on the audit process walkthrough and for sampled files, there are delays and ‘bottlenecks’ that impact the efficiency and effectiveness of certain elements of the process. Delays occur within the process at two main points: during the procurement planning process (detailed above), and at the outset of the procurement process, specifically, the time lapsed between sector request submission to PSU and request assignment, and the time required for PSU to obtain all relevant documentation from sectors. FPB management indicated that internal capacity issues impact their ability to assign requests to available procurement officers. Delays within these main process points result in additional time expended at the outset of the process, ultimately impacting and impeding the timely completion of the entire process. On April 26, 2022, updates were implemented to the eProcurement system, which require relevant information and documentation to be included when a request is submitted, instead of afterwards. These enhancements are intended to improve the efficiency of the process by eliminating the time required to obtain outstanding documentation.

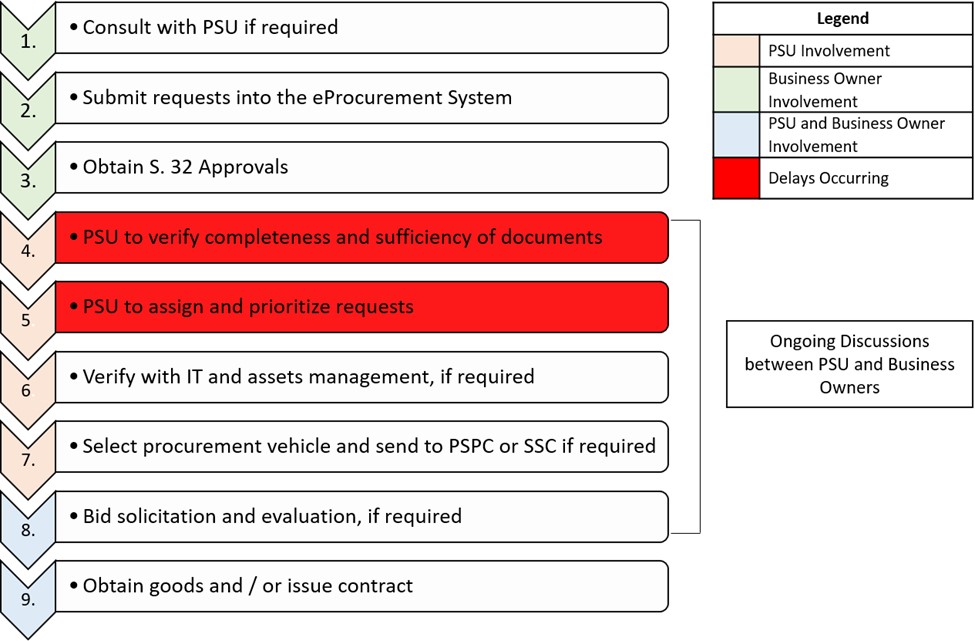

Diagram 1 – High-level Procurement Process

Diagram 1 – High-Level Procurement Process This colour-coded diagram outlines the Natural Resources Canada procurement process at a very high level. The objective of this table is to visually display the process, outline who is involved in the process and when, and to highlight where delays are occurring within the process.

A colour-coded legend is provided that defines what parties are included in a given step of the process. The colour orange indicates PSU involvement; the colour green indicates Business Owner Involvement; the colour blue indicates both PSU and Business Owner involvement; and the colour red indicates where delays are occurring within the process.

Each row represents a step within the process. There are a total of nine rows. The steps of the process include:

- Consult with PSU if required – Business Owner involvement;

- Submit requests into the eProcurement System – Business Owner involvement;

- Obtain S. 32 approvals – Business Owner involvement;

- PSU to verify completeness and sufficiency of documents – PSU involvement (delays are occurring within this step);

- PSU to assign and prioritize requests – PSU involvement (delays are occurring within this step);

- Verify with IT and assets management, if required – PSU involvement;

- Select procurement vehicle and send to PSPC or SSC if required – PSU involvement;

- Bid solicitation and evaluation, if required – PSU and Business Owners involvement; and

- Obtain good and / or issue contract – PSU and Business Owners involvement.

Finally, between steps four and eight defined above, there are ongoing discussions between PSU and Business Owners.

FPB has implemented procurement service standards, tracks and monitors this information, and reports quarterly to CMSS management on whether standards were met. Some of the information tracked internally by FPB, however, is not relevant to and does not align with the standards shared with business owners. Information shared and tracked differs based on the number of categories tracked, monetary thresholds used, and days for completion (see table below).

Table 2 – Service Standards

The target for meeting the service standard is 75%; this means that if requests are processed within the specified time frame 75% of the time, the standard has been met. During the audit scope period, service standards for all categories were met, with the exception of contracts under $25,000 for Q4 of 2020-21 (37%), and Q2 for 2021-22 (39%) and Q3 for 2021-22 (13%). This was reflected in the audit sample testing, where there were four instances where service standards were not met within the twenty-five procurement requests tested. Interviews with PSU attributed these low scores to a lack of resourcing within PSU and the challenges with the volume of requests submitted for home office and IT equipment. The audit team found that service standards information is currently used for reporting purposes, however, it has yet to be meaningfully used to address performance gaps and improve processes.

Audit interviews with business owners highlighted that the procurement process does not meet their needs due to the delays within the process. They indicated that these delays have had corresponding impacts on the achievement of business objectives and priorities. Despite the delays, overall satisfaction with the procurement process increased from 2017 to 2021, per the results of the PSU satisfaction surveys for these periods. Business owners proposed the following improvements to the procurement process during audit interviews: sharing pertinent information of outstanding procurement requests; better communicating changes to the process that have an impact on business owners and ensuring that available information is up to date; and revising guidance to ensure that it is current.

Communications in the Procurement Process

FPB utilizes a variety of mechanisms to communicate with business owners regarding procurement processes and activities, including: information on The Source; sectors engaging with their assigned sector procurement advisors; sectors completing client satisfaction surveys; business owners contacting PSU to enquire about the overall status of their requests; and business owners and the procurement officer meeting to discuss the next steps for processing their requests. The primary mechanism for communicating with sectors is The Source; however, this information is outdated and, in some cases, does not provide accurate information on procurement activities. For example, flowcharts depicting procurement processes are dated 2015, and some of the information on the procurement planning process was last updated in 2018.

The communication mechanisms utilized by FPB largely promoted one-way communication with business owners, and there are limited proactive actions taken by PSU to inform sectors of the status of their requests. Business owners interviewed indicated that often no communication with PSU will occur after request submission until the request has been assigned to a procurement officer for action. Some business owners indicated that they will proactively communicate with PSU in order to receive status updates on their procurement requests prior to request assignment.

Two-way communication primarily occurs after tickets are assigned to procurement officers for processing, and this was confirmed through audit testing. Business owners indicated that communication between them and procurement officers occurs to discuss requests, obtain missing and/or incomplete documentation, and to respond to general questions about the process. This communication provides sectors with additional information on their requests, and an understanding of file progression and expected completion.

While FPB has established mechanisms and processes in order to communicate with business owners, there is an opportunity for FPB to improve and strengthen these mechanisms and to provide all business owners with more consistent and timely communications.

When processes are not reviewed and updated regularly, there is a risk that business owners may not be equipped to efficiently and effectively execute their procurement duties, affecting the overall processing of requests and timelines, and ultimately impacting the achievement of business owner priorities and objectives.

A lack of efficient and effective procurement processes, including request prioritization, may result in delays, affecting the overall processing time and limiting the achievement of business owner priorities and objectives.

Without accurate and precise data collected and used to support the monitoring and tracking of procurement service standards, insufficient information may limit the ability to detect and remediate issues and performance gaps.

Without a consistent approach to inform business owners of the status of their requests before they are assigned and throughout the procurement process, there is a risk that the expectations for file initiation and processing time may not be clear, resulting in business owners not having the required information to make informed decisions to meet their needs and objectives.

Recommendations

Recommendation 2: It is recommended that the ADM of CMSS:

- Develop and implement a prioritization process for procurement requests, including engaging with business owners;

- Review current procurement processes to identify and analyze any procedural constraints, and devise mechanisms to promote continuous process improvement;

- Review service standards for relevance, address potential gaps in the data collected, and leverage this information to address any performance challenges; and

- Enhance communications mechanisms between contracting authorities and business owners, including assessing the feasibility of an automated mechanism to provide regular status updates throughout the procurement process and to clarify timelines.

Recommendation 3: It is recommended that the ADM of CMSS review, update, and communicate guidance to business owners, including flexibilities in procurement approaches offered in the new TB Directive, to ensure that information available is current, clear, and provides sufficient information to enable business owners to execute their duties.

Management agrees with Recommendation #2.

A: Prioritization and engagement

- FPB is working with the Financial Systems division to enhance the reporting capability within the AMI system and enhancements to eProcurement to better support and communicate to Business Owners to allow them to regularly review requests, clarify timelines, and confirm sector priorities; and to determine if additional flexibility can be built-in to improve functionality and reporting.

- FPB is developing criteria to prioritize procurement requests; i.e., prioritization amongst all the requests received from the various sectors.

- FPB has enhanced engagement between programs and procurement, for meaningful discussion and integration of procurement considerations into the planning of programs, projects and service delivery; e.g., via recurring attendance at senior management meetings and program specific discussions. Furthermore, FPB has included within the Annual Procurement Plan exercise the opportunity for sectors to prioritize their requirements. The Procurement Plan will be reviewed and updated by Business Owners at the same time as the FSRs. In addition, presentations to OC and FRPC on procurement status and progress have also occurred.

Timing : A (i) November 2022 for system, e-request and reporting enhancements; A (ii) October 2022 for prioritization criteria and recommendation process; A (iii) initiated during fourth quarter of FY 21/22 and ongoing.

B: Continuous process improvement

- FPB will be reviewing its triage/internal assignment process to find efficiencies and implement them, where feasible and will examine whether client-recalled procurements are occurring due to constraints in the process and whether an enhancement of the e-procurement system could address this issue.

- Training and awareness sessions will be developed and delivered to provide education to Business Owners on the end-to-end procurement process and legislative constraints that guide the process.

- FPB will review and streamline procurement processes as new initiatives brought forth by Central Agencies are implemented.

Timing : B (i) December 2022 for triage pilot; B (ii) May 2023 for the delivery of training; B (iii) ongoing.

C: In May 2022, a comparative analysis was undertaken to benchmark how NRCan measures against Other Government Departments (OGDs) Service Standards (e.g., GAC, PSPC, Transport, RCMP and others). This information will be leveraged to address any performance gaps and challenges. NRCan remains in line with OGD processing times based on existing analytics. While it has been challenging to consistently meet Services Standards this past FY, initiatives brought forth by Central Agencies could impact processing times (e.g., social procurement and new security requirements); as such, NRCan Procurement Service Standards will remain the same in FY 22/23, pending further assessment.

A new Service Standards Review will be conducted in September FY 23/24.

Timing : Completed and shared with senior management (via email) and FRPC members on June 7, 2022. The new Service Standards Review will be conducted in September FY 23/24. D: Enhance communications mechanisms to provide regular status updates throughout the procurement process and to clarify timelines -

- FPB has enhanced engagement between programs and procurement, for meaningful discussion and integration of procurement considerations into the planning of programs, projects and service delivery; e.g., via recurring attendance at senior management meetings and program specific discussions. In addition, FPB has included within the Annual Procurement Plan exercise the opportunity for Sectors to prioritize their requirements. The Procurement Plan will be reviewed and updated by Business Owners at the same time as the FSRs.

Timing : D (i) November 2022 for system, e-request and reporting enhancements; D (ii) completed initiated during fourth quarter of FY 21/22 and ongoing.

Management agrees with Recommendation #3.

To evolve the suite of documents already available on NRCan intranet, a client-centric web-based collaborative platform (such as SharePoint) will be developed that will house procurement guidance information, relevant notices from central agencies, required forms, service standards etc., which should provide current, clear and sufficient information to enable business owners to execute their duties. Notifications to Business Owners for updates and changes will be explored.

Timing : April 2023 for a client-centric web-based collaborative platform.

Human Resources Planning and Training

Overall, opportunities exist to formally document and strengthen HR and succession planning mechanisms for the procurement function, and associated monitoring processes. These processes are largely informal and monitoring is conducted on an ad hoc basis.

Training and guidance provided to staff are sufficient and enable staff to adequately execute their duties. However, there are opportunities to strengthen training and awareness through the addition of fraud-related and other complementary topics, and monitoring of attendance/training completion to reduce potential knowledge disparities among FPB staff.

With respect to knowledge sharing and transference in support of capacity building, there is an opportunity to ensure that mechanisms are strengthened and regularly utilized for information sharing purposes.

Effective HR and succession planning processes should be in place to support the management of procurement activities. The audit examined whether the procurement function had articulated and planned for current and future human resources needs, including the required skills, knowledge and competencies, and whether these needs were effectively implemented and monitored. Additionally, the audit examined whether those with procurement related responsibilities were equipped with adequate training, knowledge, tools and guidance necessary to fulfill their roles.

HR Planning and Succession Planning Processes

FPB leverages formal and informal processes to meet their current HR needs. Processes and mechanisms leveraged to support HR-related needs included word of mouth initiatives, utilizing pre-established resourcing pools, the Federal Internship Program for Persons with Disabilities, Student Bridging, and formally launching HR processes to seek required resources. Management indicated these processes were utilized on an ongoing basis during the audit scope period to address capacity challenges; however, in FY 2020-21 staffing processes were typically initiated once resource departures were known versus conducting them in advance. Further, management indicated that they utilize the Financial Situation Reports (FSRs) to plan for known departures and planned staffing as part of their salary forecasts.

FPB does not have formally documented succession plans in place that articulate key positions, required skills, competencies and knowledge in support of medium to long-term HR-related needs. Processes that are in place are largely informal. In addition, monitoring processes and mechanisms over HR and succession planning are conducted on an ad hoc, as needed basis.

Within PSU, formal and informal HR processes are leveraged to support and meet current HR-related needs. In this unit, there are no formally documented HR and succession plans in place. During the audit scope period, PSU indicated that there was significant turn-over within their unit; however, throughout the course of the audit, PSU was able to enhance existing resource levels by hiring 18 new full-time equivalents (FTEs). Obtaining qualified resources at the appropriate levels and having a full staff complement was noted as a challenge for PSU, who further indicated that the labour pool for procurement officers is competitive and limited. In addition, PSU recently conducted a review and revision of their Statements of Merit and Criteria (SOMCs) to ensure that defined job requirements align with current needs and activities.

Within PPAR, a formally documented HR plan exists; however, this plan is dated November 2016, and does not reflect PPAR’s current HR-related needs. A formally documented succession plan is also not in place; however, informally, PPAR has identified a successor for the PPAR Manager position. In addition, PPAR’s SOMCs are outdated; however, they indicated that there will soon be an initiative to review and update these SOMCs to reflect current needs and activities.

There is an opportunity for FPB to formalize and operationalize HR and succession plans that identify short and long-term resourcing needs. Ideally, these plans should identify key positions, and define the required skills, knowledge, and competencies required. Further, there is an opportunity for FPB to regularly monitor and review these plans to ensure that they are updated and/or actioned where required.

Training, Guidance, and Knowledge for Procurement