Profitability and working capital management: a meta-study in macroeconomic and institutional conditions

- Research Article

- Published: 14 March 2024

Cite this article

- Jacek Jaworski ORCID: orcid.org/0000-0002-6629-3497 1 &

- Leszek Czerwonka 2

111 Accesses

3 Altmetric

Explore all metrics

Working capital management (WCM) concerns decisions on the levels and turnover of the inventories, receivables, cash and current liabilities of a company. Consequently, WCM affects the profitability of an enterprise. This paper aims to determine the relationship between profitability and WCM, characterised by components of the company’s operating cycle. The research is based on meta-analysis and meta-regression methods that allow for the combination and analysis of the outcomes of individual empirical studies using statistical methods. Our final research sample consists of 43 scientific papers from 2003 to 2018. These studies covered almost 62,000 enterprises in 35 countries from 1992 to 2017. Our results indicate that there is a common, negative relationship between profitability and the cash conversion cycle (CCC). This relationship is conspicuous in various countries and in different economic contexts. A negative, statistically significant relationship was also detected between profitability and average collection period (ACP), the accounts payable period (APP) and inventory turnover cycle (ITC) as well. We also identified moderators of the diagnosed dependencies on the grounds of macroeconomic and institutional factors. The richer the economy, the weaker a negative impact of CCC on profitability. The higher the protection of creditors and debtors, the weaker the negative relationship between profitability and ITC. The opposite is applicable to inflation and ACP and APP, unemployment and CCC, ACP and APP, the availability of credit and APP and the degree of capital market development and CCC and ACP. The aforementioned macroeconomic and institutional factors cause the negative relationship between particular components of the operating cycle and profitability to deepen even further. Our research contributes to the existing knowledge by confirming that the negative relationship between profitability and all components of the operating cycle is dominant in the global economy. It also indicates that there are macroeconomic and institutional moderators of the strength and direction of these relationships.

This is a preview of subscription content, log in via an institution to check access.

Access this article

Price includes VAT (Russian Federation)

Instant access to the full article PDF.

Rent this article via DeepDyve

Institutional subscriptions

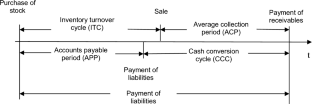

Source : Own elaboration based on (Brealey et al. 2016 )

Source : Own elaboration

Similar content being viewed by others

The impact of corporate governance on financial performance: a cross-sector study

Wajdi Affes & Anis Jarboui

Corporate entrepreneurship: a systematic literature review and future research agenda

David Urbano, Andreu Turro, … Shaker Zahra

Impact of ESG factors on firm risk in Europe

Remmer Sassen, Anne-Kathrin Hinze & Inga Hardeck

Abuzayed B (2012) Working capital management and firms’ performance in emerging markets: the case of Jordan. Int J Manag Financ 8(2):155–179. https://doi.org/10.1108/17439131211216620

Article Google Scholar

Aggarwal A, Chaudhary R (2015) Effect of working capital management on the profitability of Indian firms. IOSR J Bus Manag 17(8):34–43

Google Scholar

Ahmed K, Courtis JK (1999) Associations between corporate characteristics and disclosure levels in annual reports: a meta-analysis. British Accounting Rev. https://doi.org/10.1006/bare.1998.0082

Alavinasab SM, Davoudi E (2013) Studying the relationship between working capital management and profitability of listed companies in Tehran stock exchange. Bus Manag Dynam 2(7):1–8. https://doi.org/10.1109/TLT.2009.30

Aloe A (2014) An empirical investigation of partial effect sizes in meta-analysis of correlational data. J Gen Psychol 141(1):47–64. https://doi.org/10.1080/00221309.2013.853021

Article PubMed Google Scholar

Alshammari T (2018) International journal of economics and financial issues performance effects of working capital in emerging markets. Int J Econ Financ Issues 8(5):80–87

Aregbeyen O (2013) The effects of working capital management on profitability of Nigerian manufacturing firms. J Bus Econ Manag 14(3):520–534. https://doi.org/10.3846/16111699.2011.651626

Baños-Caballero S, García-Teruel PJ, Martínez-Solano P (2012) How does working capital management affect the profitability of Spanish SMEs? Small Bus Econ 39(2):517–529. https://doi.org/10.1007/s11187-011-9317-8

Baños-Caballero S, García-Teruel PJ, Martínez-Solano P (2019) Net operating working capital and firm value: a cross-country analysis. BRQ Bus Res Quart, Press,. https://doi.org/10.1016/j.brq.2019.03.003

Bijmolt T, Pieters R (2001) Meta-analysis in marketing when studies contain multiple measurements. Mark Lett 12(2):157–169

Blinder AS, Maccini LJ (1991) The resurgence of inventory research: What have we learned? J Econ Surv 5:291–328

Brealey RA, Myers SC, Allen F (2016) Principles of corporate finance—principles of corporate finance (12th edition), 12th edn. McGraw-Hill Education, OH

Brown S, Homer P, Inman J (1998) A meta-analysis of relationships between ad-evoked feelings and advertising responses. J Mark Res 35:114–126

Chang CC (2018) Cash conversion cycle and corporate performance: Global evidence. Int Rev Econ Financ 56:568–581. https://doi.org/10.1016/j.iref.2017.12.014

Charitou M, Lois P, Santoso HB (2012) The relationship between working capital management and firm’s profitability: a empirical investigation for an emerging Asian country. Int Bus Econ Res J 11(8):839–849

Charitou MS, Elfani M, Lois P (2016) The effect of working capital management on firm’s profitability: empirical evidence from an emerging market. J Bus Econ Res 14(3):111–118

de Jong A, Kabir R, Nguyen TT (2008) Capital structure around the world: the roles of firm-and country-specific determinants. J Bank Financ 32:1954–1969. https://doi.org/10.1016/j.jbankfin.2007.12.034

Deloof M (2003) Does working capital management affect profitability of Belgian firms? J Bus Financ Acc. https://doi.org/10.1111/1468-5957.00008

Den M, Oruc E (2009) Relationship between efficiency level of working capital management and return on total assets in ISE (Istanbul Stock Exchange). Int J Bus Manag. https://doi.org/10.5539/ijbm.v4n10p109

Ding S, Guariglia A, Knight J (2013) Investment and financing constraints in China: does working capital management make a difference? J Bank Financ. https://doi.org/10.1016/j.jbankfin.2012.03.025

Duval SJ, Tweedie RL (2000) A nonparametric `trim and fill’ method of accounting for publication bias in meta-analysis. J Am Stat Assoc 95(449):89–98

MathSciNet Google Scholar

Eljelly AMA (2004) Liquidity—profitability tradeoff: an empirical investigation in an emerging market. Int J Commer Manag 14(2):48–61. https://doi.org/10.1108/10569210480000179

Erasmus PD (2010) Working capital management and profitability: the relationship between the net trade cycle and return on assets. Manag Dyn 19(1):2–10. https://doi.org/10.1016/j.tics.2008.07.006

García-Teruel PJ, Martínez-Solano P (2007) Effects of working capital management on SME profitability. Int J Manag Financ 3(2):164–177. https://doi.org/10.1108/17439130710738718

Geyer-Klingeberg J, Hang M, Rathgeber A (2020) Meta-analysis in finance research: opportunities, challenges, and contemporary applications. Int Rev Financ Anal. https://doi.org/10.1016/j.irfa.2020.101524

Gill A, Biger N, Mathur N (2010) The relationship between working capital management and profitability: evidence from the United States. Bus Econ J 10(1):1–9

Gitman LJ (1974) Estimating corporate liquidity requirements: a simplified approach. Financ Rev. https://doi.org/10.1111/j.1540-6288.1974.tb01453.x

Glass GV (1976) Primary, secondary, and meta-analysis of research. Educ Res. https://doi.org/10.1002/hlca.200390194

Hang M, Geyer-Klingeberg J, Rathgeber AW, Stöckl S (2018) Measurement matters—a meta-study of the determinants of corporate capital structure. Quart Rev Econ Financ 68:211–225. https://doi.org/10.1016/j.qref.2017.11.011

Hanji MB (2017) Meta-analysis in psychiatry research: fundamental and advanced methods. Apple Academic Press, Toronto; New Jersey

Book Google Scholar

Hoang TV (2015) Impact of capital management on firm profitability: the case of listed manufacturing firms on Ho chi minh stock exchange. Asian Econ Financ Rev 5(5):779–789. https://doi.org/10.18488/journal.aefr/2015.5.5/102.5.779.789

Hsieh C, Chen YW (2013) Working capital management and profitability of publicly traded Chinese companies. Asian Pacyfic J Econ Bus 17(1):1–11

Jaworski J, Czerwonka L (2018) Relationship between profitability and liquidity of enterprises listed on warsaw stock exchange. In: 35th International Scientific Conference on Economic and Social Development—Sustainability from an Economic and Social Perspective Book of Proceedings (pp 15–16). https://doi.org/10.2139/ssrn.2338107

Jaworski J, Czerwonka L (2019) Meta-study on relationship between macroeconomic and institutional environment and internal determinants of enterprises’ capital structure. Econ Res-Ekonomska Istrazivanja 32(1):2614–2637. https://doi.org/10.1080/1331677X.2019.1650653

Jose ML, Lancaster C, Stevens JL (1996) Corporate returns and cash conversion cycles. J Econ Financ 20(1):33–46. https://doi.org/10.1007/BF02920497

Karaduman HA, Akbas HE, Ozsozgun A, Durer S (2010) Effects of working capital management on profitability: the case for selected companies in the Istanbul stock exchange (2005–2008). Int J Econ Financ Stud 2(2):48–54

Keskin R, Gokalp F (2016) The effects of working capital management on firm’s profitability: panel data analysis. Doğuş Üniversitesi Dergisi 17(1):15–25

Kieschnick RL, Laplante M, Moussawi R (2011) Working capital management and shareholder wealth. Rev Financ 17(5):1827–1852.

Kroes JR, Manikas AS (2014) Cash flow management and manufacturing firm financial performance: a longitudinal perspective. Int J Prod Econ. https://doi.org/10.1016/j.ijpe.2013.11.008

Kusuma H, Dhiyaullatief Bachtiar A (2018) Working capital management and corporate performance: evidence from Indonesia. J Manag Bus Administ. Central Europe, 26(2): 76–88

Lazaridis I, Tryfonidis D (2006) Relationship between working capital management and profitability of listed companies in the athens stock exchange. J Financ Manag Anal 19(l): 26–35

Li CG, Dong HM, Chen S, Yang Y (2014) Working capital management, corporate performance, and strategic choices of the wholesale and retail industry in China. Scientific World J. https://doi.org/10.1155/2014/953945

Lin TT (2015) Working capital requirement and the unemployment volatility puzzle. J Macroecon 46:201–217. https://doi.org/10.1016/j.jmacro.2015.05.006

Article CAS Google Scholar

Littell JH, Corcoran J, Pillai V (2008) Systematic reviews and meta analysis. Oxford Univ Press. https://doi.org/10.1093/acprof

Lyngstadaas H, Berg T (2016) Working capital management: evidence from Norway. Int J Manag Financ 12(3):295–313. https://doi.org/10.1108/IJMF-01-2016-0012

Mansoori E, Muhammad J (2012) The effect of working capital management on firm’s Profitability. Interdiscip J Contemporary Res Bus, pp 472–486

Mathuva DM (2010) The influence of working capital management components on corporate profitability: a survey on Kenyan listed firms. Res J Bus Manag 4(1):1–11. https://doi.org/10.3923/rjbm.2010.1.11

Michaelas N, Chittenden F, Poutziouris P (1999) Financial policy and capital structure choice in UK SMEs: evidence from company panel data. Small Bus Econ 12:113–130

Mokhova N, Zinecker M (2014) Macroeconomic factors and corporate capital structure. Procedia Soc Behav Sci 110:530–540. https://doi.org/10.1016/j.sbspro.2013.12.897

Napompech K (2012) Effect of Wcm on the profitability of thai firm. Int J Trade, Ecnomics Financ 3(3):227–232

Ng SH, Ye C, Ong TS, Teh BH (2017) The impact of working capital management on firm’s profitability: evidence from Malaysian listed manufacturing firms. Int J Econ Financ Issues 7(3):662–670. https://doi.org/10.11114/afa.v4i1.2949

Nobanee H, Abdullatif M, Alhajjar M (2011) Cash conversion cycle and firm’s performance of Japanese firms. Asian Rev Account 19(2):147–156. https://doi.org/10.1108/13217341111181078

North D (1990) Institutions, institutional change and economic performance. Harvard University Press, Cambridge

Nyamweno CN, Olweny T (2014) Effect of working capital management on performance of firms listed at the Nairobi securities exchange. Econ Financ Rev 3(11):1–14

Padachi K (2006) Trends in working capital management and its impact on firms’ performance: an analysis of Mauritian small manufacturing firms. Int Rev Bus Res Papers 2(2):45–58

Pais MA, Gama PM (2015) Working capital management and SMEs profitability: Portuguese evidence. Int J Manag Financ 11(3):341–358. https://doi.org/10.1108/IJMF-11-2014-0170

Peterson R (1994) A meta-analysis of Cronbach’s coefficient alpha. J Consumer Res 21:381–391

R Core Team (2019) R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. https://www.R-project.org/

Raheman A, Afza T, Qayyum A, Bodla M (2010) Working capital management and corporate performance of manufacturing sector in Pakistan. Int Res J Financ Econ 47(1):156–169

Rosenthal R (1991) Meta-analytic procedures for social research. Sage, Newbury Park

Ross S, Westerfield RW, Jordan BD (2013) Fundementals of corporate finance 10e. In McGraw-Hill Irwin, New York

Saldanli A (2012) The relationship between liquidity and profitability—an empirical study on the ISE-100 manufacturing sector. J Suleyman Demirel Univ Inst Soc Sci 16:167–176

Şamiloğlu F, Akgün Aİ (2016) The relationship between working capital management and profitability: evidence. Bus Econ Res J 7(2):1–14

Schmidt FL, Hunter JE (2004) Methods of meta-analysis: correcting error and bias in research findings. In: Methods of Meta-Analysis: Correcting Error and Bias in Research Findings (2nd edition). Thousand Oaks. https://doi.org/10.4135/9781483398105

Sethuraman R (1995) A meta-analysis of national brand and store brand cross-promotional price elasticities. Mark Lett 6(4):275–286

Shelby LB, Vaske J (2008) Understanding meta-analysis: a review of the methodological literature. Leis Sci. https://doi.org/10.1080/01490400701881366

Shin H-H, Soenen L (1998) Efficiency of working capital management and corporate profitability. Financ Pract Educ 8(2):37–45. https://doi.org/10.1002/(SICI)1099-0518(20000515)38:10%3c1753::AID-POLA600%3e3.0.CO;2-O

Shrivastava A, Kumar N, Kumar P (2017) Bayesian analysis of working capital management on corporate profitability: evidence from India. J Econ Stud 44(4):568–584. https://doi.org/10.1108/JES-11-2015-0207

Singh HP, Kumar S, Colombage S (2017) Working capital management and firm profitability: a meta-analysis. Qualitat Res Financ Mark 9(1):34–47. https://doi.org/10.1108/QRFM-06-2016-0018

Smith K (1980) Profitability versus liquidity tradeoffs in working capital management. In: Smith K (ed) Readings on the management of working capital. West Publishing Company, St. Paul, pp 549–562

Smith JK (1987) Trade credit and informational asymmetry. J Financ 42:863–872

Suurmond R, van Rhee H, Hak T (2017) Introduction, comparison, and validation of meta-essentials: a free and simple tool for meta-analysis. Res Synthesis Methods. https://doi.org/10.1002/jrsm.1260

Tauringana V, Adjapong Afrifa G (2013) The relative importance of working capital management and its components to SMEs’ profitability. J Small Bus Enterp Dev 20(3):453–469. https://doi.org/10.1108/JSBED-12-2011-0029

Tran H, Abbott M, Jin Yap C (2017) How does working capital management affect the profitability of Vietnamese small-and medium-sized enterprises? J Small Bus Enterp Dev 24(1):2–11. https://doi.org/10.1108/JSBED-05-2016-0070

Troilo M, Walkup BR, Abe M, Lee S (2019) Legal systems and the financing of working capital. Int Rev Econ Financ 64:641–656. https://doi.org/10.1016/j.iref.2018.01.010

Ugurlu E, Jindrichovska I, Kubickova D (2014) Working capital management in Czech SMEs : an econometric approach. Procedia Econ Business Administrat, pp 311–317

Ukaegbu B (2014) The significance of working capital management in determining firm profitability: evidence from developing economies in Africa. Res Int Bus Financ 31:1–16. https://doi.org/10.1016/j.ribaf.2013.11.005

Vahid TK, Elham G, Mohsen A, khosroshahi, Mohammadreza, E (2012) Working capital management and corporate performance: evidence from Iranian companies. Procedia Soc Behav Sci 62:1313–1318. https://doi.org/10.1016/j.sbspro.2012.09.225

Valipour H, Jamshidi A (2012) Determining the optimal efficiency index of working capital management and its relationship with efficiency of assets in categorized industries: evidence from Tehran stock exchange ( TSE ). Adv Manag Appl Econ 2(2):191–209

Viechtbauer W (2010) Conducting meta-analyses in R with the metafor package. J Statist Softw 36(3):1–48

Vural G, Sokmen AG, Cetenak E (2012) Affects of working capital management on firm’s performance: evidence from Turkey. Int J Econ Financ Issues 2(4):488–495

Wöhrmann A, Knauer T, Gefken J (2012) Kostenmanagement in Krisenzeiten: rentabilitätssteigerung durch working capital management? Zeitschrift Für Controll Manag 56:83–88. https://doi.org/10.1365/s12176-012-0649-2

Yazdanfar D, Öhman P (2014) The impact of cash conversion cycle on firm profitability: an empirical study based on Swedish data. Int J Manag Financ 10(4):442–452. https://doi.org/10.1108/IJMF-12-2013-0137

Yunos RM, Nazaruddin N, Ghapar FA, Ahmad SA, Zakaria NB (2015) Working capital management in Malaysian government-linked companies. Procedia Econ Financ 31(15):573–580. https://doi.org/10.1016/S2212-5671(15)01203-4

Download references

There are no special grants and institutions supporting submitted study.

Author information

Authors and affiliations.

Faculty of Business, WSB Merito University in Gdańsk, Al. Grunwaldzka 238A, 80-266, Gdańsk, Poland

Jacek Jaworski

Faculty of Economics, University of Gdańsk, ul. Armii Krajowej 119, 81-824, Sopot, Poland

Leszek Czerwonka

You can also search for this author in PubMed Google Scholar

Contributions

Both authors contributed to the study conception and design. JJ is especially responsible for literature review and research question and hypotheses formulation, whereas LC for empirical study elaboration. Discussion and conclusions are the results of common work.

Corresponding authors

Correspondence to Jacek Jaworski or Leszek Czerwonka .

Ethics declarations

Conflict of interest.

The authors have no relevant financial or non-financial interests to disclose.

Additional information

Publisher's note.

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Source : Own elaboration (in metafor R package)

Funnel plots of standard error by partial correlation coefficient (Fisher’s z transformed) ratio for studies included in meta-analysis (after trimming and filling).

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

Reprints and permissions

About this article

Jaworski, J., Czerwonka, L. Profitability and working capital management: a meta-study in macroeconomic and institutional conditions. Decision (2024). https://doi.org/10.1007/s40622-023-00372-x

Download citation

Accepted : 08 December 2023

Published : 14 March 2024

DOI : https://doi.org/10.1007/s40622-023-00372-x

Share this article

Anyone you share the following link with will be able to read this content:

Sorry, a shareable link is not currently available for this article.

Provided by the Springer Nature SharedIt content-sharing initiative

- Meta-analysis

- Profitability

- Working capital management

- Cash conversion cycle

- Meta-regression

- Macroeconomic and institutional factors

- Find a journal

- Publish with us

- Track your research

Working capital management: a literature review and research agenda

Purpose – The purpose of this paper is to review research on working capital management (WCM) and to identify gaps in the current body of knowledge, which justify future research directions. WCM has attracted serious research attention in the recent past, especially after the financial crisis of 2008. Design/methodology/approach – Using systematic literature review (SLR) method, the present study reviews 126 articles from referred journal and international conferences published on WCM. Findings – Detailed content analysis reveals that most of the research work is empirical and focuses mainly on two aspects, impact of working capital on profitability of firm and working capital practices. Major research work has concluded that WCM is essential for corporate profitability. The major issues with prior literature are lack of survey-based approach and lack of systematic theory development study, which opens all new areas for future research. The future research directions proposed in this paper may help develop a greater understanding of determinants and practices of WCM. Practical implications – Till date, literature on classification of WCM has been almost non-existent. This paper reviews a large number of articles on WCM and provides a classification scheme in to various categories. Subsequently, various emerging trends in the field of WCM are identified to help researchers specifying gaps in the literature and direct research efforts. Originality/value – This paper contains a comprehensive listing of publications on the WCM and their classification according to various attributes. The paper will be useful to researchers, finance professionals and others concerned with WCM to understand the importance of WCM. To the best of the authors’ knowledge, no detailed SLR on this topic has previously been published in academic journals.

- Related Documents

A systematic literature review on working capital management – an identification of new avenues

Purpose This paper aims to provide a review of the existing literature available on working capital (WC) and working capital management (WCM). Design/methodology/approach A systematic literature review (SLR) methodology is used to review 187 articles selected from referred journals, books and international conferences for the period 1980-2017. Findings This comprehensive review reveals that much of the focus in the existing literature is paid on investigating the empirical relationship between WCM and firm performance. Furthermore, the attention has been paid towards studying the WC practices. The behavioural aspects, qualitative studies, survey studies and systematic theory development have been ignored in most of the prior studies. These areas have a broader scope for future research. Research limitations/implications This study is based on literature review and theoretical in nature. Therefore, it does not have any empirical results. Practical implications So far, a limited literature review studies have been conducted in WCM perspective. This review provides various emerging trends, which may be considered in future research for providing a deep understanding of WCM. Originality/value This is the first time a detailed review of WCM literature has been conducted by using SLR for the period of 1980-2017. This review will be useful for researchers, business policymaker, finance professionals and all other having direct or indirect concerns with WCM study.

Process improvement project failure: a systematic literature review and future research agenda

Purpose Although scholars have considered the success factors of process improvement (PI) projects, limited research has considered the factors that influence failure. The purpose of this paper is to extend the understanding of PI project failure by systematically reviewing the research on generic project failure, and developing research propositions and future research directions specifically for PI projects. Design/methodology/approach A systematic literature review protocol resulted in a total of 97 research papers that are reviewed for contributions on project failure. Findings An inductive category formation process resulted in three categories of findings. The first category are the causes for project failure, the second category is about relatedness between failure factors and the third category is on failure mitigation strategies. For each category, propositions for future research on PI projects specifically are developed. Additional future research directions proposed lay in better understanding PI project failure as it unfolds (i.e. process studies vs cross-sectional), understanding PI project failure from a theoretical perspective and better understanding of PI project failure antecedents. Originality/value This paper takes a multi-disciplinary and project type approach, synthesizes the existing knowledge and reflects upon the developments in the field of research. Propositions and a framework for future research on PI project failure are presented.

Research in urban logistics: a systematic literature review

Purpose The last decades have witnessed an increased interest in urban logistics originating from both the research and the practitioners’ communities. Sustainable freight transports today are on the political, social and technological agenda of many actors operating in urban contexts. Due to the extent of the covered areas and the continuous progress in many fields, the resulting body of research on urban logistics appears quite fragmented. From an engineering management perspective, the purpose of this paper is to present a systematic literature review (SLR) that aims to consolidate the knowledge on urban logistics, analyse the development of the discipline, and provide future research directions. Design/methodology/approach The paper discusses the main evidence emerging from a SLR on urban logistics. The corpus resulting from the SLR has been used to perform a citation network analysis and a main path analysis that together underpin the identification of the most investigated topics and methodologies in the field. Findings Through the analysis of a corpus of 104 articles, the most important research contributions on urban logistics that represent the structural backbone in the development of the research over time in the field are detected. Based on these findings, this work identifies and discusses three areas of potential interest for future research. Originality/value This paper presents an SLR related to a research area in which the literature is extremely fragmented. The results provide insights about the research path, current trends and future research directions in the field of urban logistics.

Green competencies: insights and recommendations from a systematic literature review

PurposeThis study conceptualises the construct – green competencies. The concept is in the niche stage and needs further elaboration. Hence, to address the research gap, this study follows the steps proposed by Tranfield et al. (2003). The major part of the study comprises descriptive analysis and thematic analysis. Descriptive analysis of the selected 66 articles was examined with the classification framework, which contains year-wise distribution, journal-wise distribution, the focus of the concept, the economic sector, and dimensions of sustainable development. The paper conducts a thematic analysis of the following research questions. What are the green competencies and their conceptual definition? What are their dimensions?Design/methodology/approachThis paper applies a systematic literature review of green competencies literature, extends the state-of-the-art using the natural resource-based view, and discusses future research directions for academicians and practitioners.FindingsIn recent years, there was considerable interest in green competencies (GC), as reflected in the surge of articles published in this genre. This paper asserts that green competencies are a multidimensional construct comprised of green knowledge, green skills, green abilities, green attitudes, green behaviours, and green awareness.Originality/valueDespite the significance of green competencies, there has been a dearth of study to define the constructs and identify the dimensions. Hence, this study addresses the literature gap by conceptualisation and discusses dimensions of the construct.

Nexus between business process management (BPM) and accounting

Purpose Multidisciplinary business process management (BPM) research can reap significant impact. We can particularly benefit from incorporating accounting concepts to address some of the key BPM challenges, such as value-creation and return on investment of BPM activities. However, research which addresses a relationship between BPM and accounting is scarce. The purpose of this paper is to provide a detailed synthesis of the current literature that has integrated accounting aspects with BPM. The authors profile and thematically describe existing research, and derive evidence-based directions to guide future research. Design/methodology/approach A multi-staged structured literature review approach to search for the two broad themes, accounting and BPM, supported by NVivo (to manage the papers and the coding and analysis processes) was designed and followed. Findings The paper confirms the dearth of work that ties the two disciplines, despite the synergetic multidisciplinary results that can be attained. Available literature is mostly from the management accounting perspective and relates to describing how performance management, in particular performance measurement, can be applicable to process improvement initiatives together with tools such as activity-based costing and the balanced scorecard. There is a lack of research that examines BPM in relation to any financial accounting perspectives (such as external reporting). Future research directions are proposed together with implications for practitioners with the findings of this structured literature review. Research limitations/implications The paper provides a detailed synthesis of the existing literature on the nexus between accounting and BPM. It summarizes the implications for practitioners and provides directions for future research by identifying key gaps and opportunities with a sound contextual basis for extension and new work. Originality/value Effective literature reviews create strong foundations for future research and accumulate the otherwise scattered knowledge into a single place. This is the first structured literature review that provides a detailed synthesis of the research that ties together the accounting and BPM disciplines, providing a basis for future research directions together with implications for practitioners.

Organizational learning and Industry 4.0: findings from a systematic literature review and research agenda

PurposeIndustry 4.0 has been one of the most topics of interest by researches and practitioners in recent years. Then, researches which bring new insights related to the subjects linked to the Industry 4.0 become relevant to support Industry 4.0's initiatives as well as for the deployment of new research works. Considering “organizational learning” as one of the most crucial subjects in this new context, this article aims to identify dimensions present in the literature regarding the relation between organizational learning and Industry 4.0 seeking to clarify how learning can be understood into the context of the fourth industrial revolution. In addition, future research directions are presented as well.Design/methodology/approachThis study is based on a systematic literature review that covers Industry 4.0 and organizational learning based on publications made from 2012, when the topic of Industry 4.0 was coined in Germany, using data basis Web of Science and Google Scholar. Also, NVivo software was used in order to identify keywords and the respective dimensions and constructs found out on this research.FindingsNine dimensions were identified between organizational learning and Industry 4.0. These include management, Industry 4.0, general industry, technology, sustainability, application, interaction between industry and the academia, education and training and competency and skills. These dimensions may be viewed in three main constructs which are essentially in order to understand and manage learning in Industry 4.0's programs. They are: learning development, Industry 4.0 structure and technology Adoption.Research limitations/implicationsEven though there are relatively few publications that have studied the relationship between organizational learning and Industry 4.0, this article makes a material contribution to both the theory in relation to Industry 4.0 and the theory of learning - for its unprecedented nature, introducing the dimensions comprising this relation as well as possible future research directions encouraging empirical researches.Practical implicationsThis article identifies the thematic dimensions relative to Industry 4.0 and organizational learning. The understanding of this relation has a relevant contribution to professionals acting in the field of organizational learning and Industry 4.0 in the sense of affording an adequate deployment of these elements by organizations.Originality/valueThis article is unique for filling a gap in the academic literature in terms of understanding the relation between organizational learning and Industry 4.0. The article also provides future research directions on learning within the context of Industry 4.0.

Islamic social finance: a literature review and future research directions

Purpose This paper aims to study the main trends of scientific research in Islamic finance’s social aspects to clarify place, role and functions, especially in the context of increasing social problems. To achieve this goal, this paper focuses on the social component of Islamic finance, analyzes publications on social Islamic finance in the Web of Science database, covering the period from 1979 to 2020, specify the geographical localization of research networks, determines the most cited authors and their scientific position. Design/methodology/approach The authors have applied several literature review techniques, a bibliometric citation and co-citation analysis, a co-authorship analysis and a review of the most cited papers. The analyzes’ results allow us to offer five future questions in Islamic social finance, zakat and waqf, which have not been investigated before and could influence Islamic social finance and Islamic finance research. Findings The authors also derive and summarize five leading future research questions. Research limitations/implications This is a limitation of using only the Web of Science Core Collection database as the premier resource and the most trusted citation index for the world’s scientific and scholarly research. Further study might expand the types of analyzed units, include more keywords and include other databases, such as Scopus. Originality/value This paper can be considered as an inspirational one to future researchers and policymakers in Islamic social finance.

Defined strategies for financial working capital management

Purpose – The purpose of this paper is to develop strategies for financial working capital management and to present previous literature on financial working capital management and its measures. Design/methodology/approach – Qualitative comparative analysis is used to formulate the strategies, and the variables in the analysis have been selected from previous literature. Empirical data consists of 91 companies listed in the Helsinki Stock Exchange during 2008-2012. Findings – The results indicate 11 possible strategies for financial working capital management which all aim at increasing financial working capital. There are suitable strategies for all companies independent from their profitability, capital intensity or working capital requirements. Research limitations/implications – The presented strategies have been created theoretically and have not been tested in companies, which could be done in future research. Originality/value – This study has three contributions. First, previous literature on financial working capital management is reviewed. Second, a novel measure for financial working capital is developed. Third, strategies for financial working capital management are presented.

Life cycle assessment of anaerobic digestion systems

Purpose It is well known that sustainability is the ideal driving path of the entire world and renewable energy is the backbone of the ongoing initiatives. The current topic of argument among the sustainability research community is on the wise selection of processes that will maximize yield and minimize emissions. The purpose of this paper is to outline different parameters and processes that impact the performance of biogas production plants through an extensive literature review. These include: comparison of biogas plant efficiency based on the use of a diverse range of feedstock; comparison of environmental impacts and its reasons during biogas production based on different feedstock and the processes followed in the management of digestate; analysis of the root cause of inefficiencies in the process of biogas production; factors affecting the energy efficiency of biogas plants based on the processes followed; and the best practices and the future research directions based on the existing life cycle assessment (LCA) studies. Design/methodology/approach The authors adopted a systematic literature review of research articles pertaining to LCA to understand in depth the current research and gaps, and to suggest future research directions. Findings Findings include the impact of the type of feedstock used on the efficiency of the biogas plants and the level of environmental emissions. Based on the analysis of literature pertaining to LCA, diverse factors causing emissions from biogas plants are enlisted. Similarly, the root causes of inefficiencies of biogas plants were also analyzed, which will further help researchers/professionals resolve such issues. Findings also include the limitations of existing research body and factors affecting the energy efficiency of biogas plants. Research limitations/implications This review is focused on articles published from 2006 to 2019 and is limited to the performance of biogas plants using LCA methodology. Originality/value Literature review showed that a majority of articles focused mainly on the efficiency of biogas plants. The novel and the original aspect of this review paper is that the authors, alongside efficiency, have considered other critical parameters such as environmental emission, energy usage, processes followed during anaerobic digestion and the impact of co-digestion of feed as well. The authors also provide solid scientific reasoning to the emission and inefficiencies of the biogas plants, which were rarely analyzed in the past.

High-performance organization: a literature review

PurposeThis paper aims to review and synthesize notable literature on high-performance organization (HPO), from which future research directions can be recommended.Design/methodology/approachThis narrative literature review analyzes major HPO literature in popular books and peer-reviewed articles published in English in the period between 1982 and 2019.FindingsThe review revealed that HPO literature has evolved multiple times, illustrating the complex and multifaceted nature of this phenomenon. In particular, literature on HPO has evolved in four phases: (1) definitions and conceptual development of HPO; (2) exploration of approaches to achieve HPO; (3) empirical validation of HPO framework; and (4) complicated research models and designs on HPO. Several research gaps were identified, which definitely hold varying research value and can be seen as potential opportunities for future research.Research limitations/implicationsThe focus of this review is on HPO literature published in English rather than cover all existing literature.Originality/valueIt is among the first studies to review the HPO literature and its evolution. This review also recommends constructive areas for future research on HPO to focus on.

Export Citation Format

Share document.

Role of working capital management in profitability considering the connection between accounting and finance

Asian Journal of Accounting Research

ISSN : 2459-9700

Article publication date: 25 August 2020

Issue publication date: 7 December 2020

The study aims to explain the relationship between accounting and finance through measuring the effect of rational working capital management on profitability.

Design/methodology/approach

Employing the methodology of semi-structured interviews with sixteen financial managers.

The findings pointed out the relationship between accounting and finance is complementary, since it supports the accountant by the critical skills and information, like project evaluation, managing the company funding resources and working capital management. These skills put the accountant up to the financial manager stage. The working capital investment and financing policies have the most significant impact on profitability. These policies related to risk and return theory; since the conservative policy will reduce both the risk and return and the aggressive one will have the opposite impact.

Originality/value

It recommends accountants to be in professional stage and increase the profitability of the company to grab both accounting and finance information and skills.

- Working capital

- Profitability

- M4 Accounting and Auditing

Morshed, A. (2020), "Role of working capital management in profitability considering the connection between accounting and finance", Asian Journal of Accounting Research , Vol. 5 No. 2, pp. 257-267. https://doi.org/10.1108/AJAR-04-2020-0023

Emerald Publishing Limited

Copyright © 2020, Amer Morshed

Published in Asian Journal of Accounting Research . Published by Emerald Publishing Limited. This article is published under the Creative Commons Attribution (CC BY 4.0) licence. Anyone may reproduce, distribute, translate and create derivative works of this article (for both commercial and non-commercial purposes), subject to full attribution to the original publication and authors. The full terms of this licence may be seen at http://creativecommons.org/licences/by/4.0/legalcode

1. Introduction

Despite the strong correlation between accounting and finance, each of them influences the management of operations in a different direction ( Brief and Peasnell, 2013 ). This link leads some people, who are not experienced and do not have the relevant knowledge, to confuse these two terms and connect some unrelated job duties to accountants ( Droms and Wright, 2010 ). Cleary and Quinn (2016) mentioned that accounting is an essential component of financing operations since finance is a term that includes accounting information.

Thus, the information provided by accountants is the primary element in decisions made by managers in general and financial managers in particular. However, in this context, Fields (2016) added that financing incorporates more subjects than only accounting. It contains statistics, economics, mathematics and any matters which are required for financing.

The main objective of the company, in common, is to achieve the most significant profits. The company aims to gain the maximum profit, and this can be done by multiplying the volume of production or the operation. One of the essential portions of production, trading and providing service is the working capital. Therefore, companies provide liquidity for working capital to achieve business continuity. In obtaining the purposes of the company, most often, business and financial directors are entitled to implement relevant working capital management policies. These policies are needed for financing because errors in working capital management may lead the commercial operations to withdrawn. Consequently, the sequence follows up on the status of working capital. It is significant and in touch with the entire business position ( Muhammad et al. , 2016 ).

Accordingly, the study aims to explain the relationship between accounting and finance through measuring the effect of rational working capital management on profitability and discussing the financial managers' responsibility. This article applies different procedures than those applied by other studies related to working capital management. The methodology adopts the qualitative method by conducting interview via Skype with financial managers from various territories in Europe and Asia to collect the data. These data reflect the best practices of working capital management from different economies, industries and sizes of capital. Hence, the results will be more generalisable.

The article found that the corporate finance skills put the accountant up to the financial manager stage. The working capital models play a significant role in advancing the profitability. Moreover, investment and financing policies have a substantial impact on profitability. These policies are related to risk and return theory since the balance between conservative and aggressive policies will contribute positive results.

Section 2 discusses a literature review of the working capital management. Section 3 discusses the methodology. Section 4 is the findings and discussion. In the end, Section 5 points out the conclusion.

2. Literature review

Explaining the profitability importance, Cakici et al. (2017) concluded that the companies use profitability as one of the four segments applied for the analysis of financial statements and performance. The other three are efficiency, solvency and market prospects. Managers, creditors and investors use these crucial impressions to analyse the company performance and its future potential if operations are suitably achieved. Vintilă and Nenu (2016) added that resources such as cash, overdraft and liabilities are used to cover the variable and fixed costs of the production process and to purchase the stock for resale operations. Profitability is the relationship between revenue and expenses and how well the company is performing and the potential future growth of the company and how it manages its working capital.

To explore the working capital management's effects on the profitability, Anwar (2018) examined the influence of the length of the operation cycle and the turnover of receivables and inventory on the profitability index of listed firms in Indonesia. The article concluded that reducing the turnover of both receivables and inventory leads to a decrease in the operation cycle and an increase the companies' profitability. Lazaridis and Tryfonidis (2006) reached results which show a relation between profitability and the operating cycle. Further, directors are able to generate gains for their businesses by controlling the operating cycle carefully and maintaining every different factor of the working capital to the most appropriate level. Pais and Gama (2015) pointed out many outcomes that inform the drop in the period of collecting the trade receivables and the rise in the number of days to settle their commercial liabilities are related to higher profitability. Additionally, the profitability is also an advance in return on assets with a reduction of the working capital amount.

The role of working capital management policies arose when Padachi (2006) concluded that excellent working capital control and policy affect the formulation of a company's value. This conclusion came from the investigation of the working capital control policy objectives and its relation to companies' achievement and profitability. This was done by applying statistical methods using the return on total assets ratio. The results show that focussing heavily on investments in high capital causes low profitability ratios. Muhammad et al. (2016) added that firms can use working capital management, which is one of the essential determinants to influence their profitability. The result reveals that there is an association between working capital elements and profitability. This is defined as the increase in the cash conversion cycle influences the profitability negatively. Additionally, directors can produce a definite amount for the company by minimising the cash conversion cycle at the most suitable level and performing a proper working capital policy and by taking care of each element of it at a sharp level. The findings of the study of Singh et al. (2017) confirmed that working capital management is linked with profitability, which indicates that aggressive working capital investment and finance policies drive higher profitability. Moreover, the cash conversion cycle is observed to be related to profitability negatively. The paper examined the working capital management variations and profitability by analysing the connection among changes in working capital management and firm profitability.

The previous literature review provides evidence of the significant roles of working capital management on the accounting profitability and assures that both accounting and finance are strongly associated. This article will apply different procedures than those applied in other studies related to working capital management to provide a deep discussion of the role of working capital management in profitability with the connection between accounting and finance.

3. The methodology

Aiming to approach practical information related to the study purpose and find practical generalised implications, this paper examines the opinions of interviewees gathered from semi-structured interviews with a group of participants consisting of sixteen financial managers. All the interviewed persons are actively involved in the financial decisions of their companies. Those interviewed found a strong desire to study objects and thus produced a fruitful penetration in this article. The respondents were selected depending on the country, industry and the size of capital as in the following table (see Table 1 ):

The researcher conducted semi-structured interviews to gain relevant data for the research objective. The meetings were carried within a reasonably free connection. Therefore, some questions proposed were not planned. Only the main questions to start the conversation were planned.

Numerous questions were automatically asked through the interview, providing elasticity to both the interviewer and the participant. This elasticity helped to examine and explain additional features or to recognise other vital details. This is unlike a structured interview, where questions are designed and arranged beforehand.

The key questions of the interviews were:

Do you find corporate finance important to accounting?

How do working capital management models improve profitability?

How do working capital management policies affect the profitability?

The meetings were in the structure of a dialogue. The interviews were conducted via Skype during the period of May 2019 until February 2020. The meetings were in Arabic and English, and the Arabic interviews were translated into English. They were recorded, transcribed and coded manually by the researcher. Finally, the researcher compared the interview proceeds with related literature in order to find the results.

The method proceeded by including the analysis of discussion records and applying qualitative coding and manual recoding by the researcher. This technique depends on the researcher's qualifications of the subject since the researcher has an eleven years' experience in accounting and auditing and, additionally, professional certificates in accounting.

4. Findings and implications

For the purpose of exploring the connection between the accounting and finance, the conversation started by the question:

4.1 Do you find corporate finance important to accounting?

If you do not understand how to use corporate finance, you will pass as a simple accountant. It is called financial management. How can any manager take a financial decision without it?.

Accordingly, using hermeneutic analysis, financial management supports and advances the accountant to be a financial manager.

I have completed my master's degree in accounting and finance, and there were two compulsory subjects related to corporate finance. There are many universities that have departments named finance and accounting, that means the instructors have information on both accounting and finance.

I am a CMA holder; the second part of this certificate is ultimately about corporate finance. The association of chartered certified accountant providing the ACCA, and this certificate include two critical papers about corporate finance which are financial management and advanced financial management.

These abstracted sentences provide tangible evidence for the connection between accounting and finance. This realisation came from the point that professional accounting bodies consider financial management as an essential part in their certifications.

On the other hand, the participants provided valuable information related to accounting education. Universities provide the junior accountant to the market. Therefore, they should consider the financial management as a vital part of the accounting curriculum that improves the new graduates' skills.

Investment decision skills

The previous literature shows that investment decision skills are essential for the accountant to be a financial manager. They point out some of these skills, like the net present value (NPV), internal rate of return (IRR), payback method and the equivalent annual cost method ( Gardiner and Stewart, 2000 ; Hung and Liu, 2005 ; Daunfeldt and Hartwig, 2014 ).

Imaging yourself in a meeting with the CEO, and he asks you to appraise a project. Without investment appraisal skills, you are in an embarrassing situation. As a financial manager at a manufacturing company, I have to decide when the underlying machine should be replaced. Therefore, I use the equivalent annual cost method since it could be applied to compute a maximum replacement cycle.

Where I work, we do many projects in one year, and it is essential to predict the profitability of these projects and the time when the initial cost payback, so you have to be familiar with the NPV and payback methods.

I know many accountants are still doing the usual accounting occupation since they do not have investment appraisal skills like NPV and IRR.

(2)Funding from external sources

Many ways to source funds from external resources were mentioned during conversations, like bonds, deep discount bonds, convertible bonds and long-term bank loans ( Kiyama and Rios-Aguilar, 2017 ).

It is valuable to each accountant to be a professional financial manager to know how he can find the sources of funds for the company; especially the external funds. There are many types of funds available for any firm; some of them are internal and others are external, but the vital thing for the financial decision is the gearing. If you are a professional financial manager, you have to keep the WACC in optimal value.

The researcher, using hermeneutic analysis with meeting proceeds, found that gearing and capital structure have a vital impact on profitability. Four theories explain this impact. The quoted sentences were identical to the literature. Therefore, both were combined to avoid redundant wording.

Traditional view: Under the traditional view, the ideal capital combination leads to minimising the average cost of capital. The cost of debt remains fixed up to a particular percentage of gearing. Passing this scale leads to a higher debt cost. The financial risk increase if gearing raises this relationship causes the equity cost to increase ( Berry et al. , 1993 ).

Modigliani and Miller (MM): The firm operating level and its profits only specify the market value of the firm in the position of no tax. The risk is attached to these profits, so there is no relation to the gearing. In the case of tax, a high level of gearing decreases the cost of capital since the interest is taxable. ( Brusov et al. , 2011 ).

Market imperfections: In a high level of gearing, the company is unable to perform its interest obligation, leading to bankruptcy ( Sanstad and Howarth, 1994 ).

Pecking order theory: Firms favour retained earnings as the optimal source of finance and then straight debt, convertible debt, preference shares and equity shares ( De Jong et al. , 2011 ).

To discuss the second key question:

4.2 How do working capital management models improve profitability?

The participators mentioned that working capital management deals with the root of the operation and the daily transactions that include cash, receivables, trade payables and inventory.

Da Costa Moraes et al. (2015) and Righetto et al. (2016) mentioned that the Baumol model and the Miller–Orr model are critical to run the cash in the optimal value to keep the liquidity and earn a profit.

(4)Inventory

Previous studies mentioned the impact of inventory management on profitability and showed that models are being used to improve inventory management.

Economic order quantity:

The professional stock administration can be divided into three sections: (EOQ), discounts for bulk purchases, it could be more economical to purchase inventories in significant order quantities to achieve discounts, buffer inventories to reduce the stock-out risk.

(EOQ) is the ordering amount for an inventory item which reduces the costs of stocking and damage.

Just-in-time system:

(5)Accounts receivable

Braun et al. (2018) supported that a higher balance of bad debt improves sales size. Given that, when the progress of the sales passes the total addition to the cost of fixed expenses and bad debts and discounts, the policy of mitigating credit requirements is profitable.

Providing credit possesses a cost; the amount of the interest imposed on an overdraft to finance the credit time; additionally, the not collected cash misses the interest of the bank deposit. Improvement in profit of increased sales following from granting credit could balance this loss.

One of the methods mentioned to keep the accounts receivable as a profitable behaviour is a credit rating system.

Credit score:

Ajanaku and Ekundayo (2017) and Richard and Kabala (2019) mentioned that points are granted according to client efficiency components, the credit amount relay on their credit score.

The interviews contributed that “the institution may establish a credit rating scheme for different customers based on personal client characteristics (such as whether the client is the owner of a state, the customer, age and profession).”

The second method is factoring; it was coded from the transcript of many interviews.

Factoring is an agreement to possess debts gathered by a factoring firm, which prepays a balance of the money it is due to settle ( Van der Vliet et al. , 2015 ).

(6)Trade accounts payable

Attempting to receive a satisfying credit of suppliers. Endeavouring to enlarge credit times of cash deficit. Keeping relations with frequent and significant suppliers.

Accordingly, the researcher comprehended from the interviews that these models of working capital management are effective since almost the entire sample apply them.

The third key question during the meetings was:

4.3 How do working capital management policies affect the profitability?

(7)Working capital investment policy

Organisations must ascertain the significant risks linked to working capital and hence whether to adopt a conservative, aggressive or moderate method to investing in working capital.

The conservative working capital investment policy aims to decrease the risk of operation failure by maintaining high levels of working capital.

The aggressive working capital investment strategy aims to overcome this financing cost and improve profitability. That could be by using the method of lowering inventories, advancing recovering credit time of customers and lingering instalments to suppliers.

(8)Working capital financing policy

Working capital financing policies are divided into conservative, aggressive and moderate approaches to financing working capital. It is classified according to the size of working capital financing from short-term assets and long-term assets ( Mohamad and Saad, 2010 ; Wasiuzzaman and Arumugam, 2013 ; Kwenda and Holden, 2014 ).

Almost all the participators expressed the opinion “the relation between the selected policy and the profitability is ‘high-risk, high-return’”. That means that aggressive policies increase profitability. This opinion is supported by ( Pais and Gama, 2015 ; Baños-Caballero et al. , 2016 ; Gonçalves et al. , 2018 ; Chand et al. , 2019 ).

On the other hand, opinions expressed based on practical experiences prefer the moderate policies, “moderate policies meet the targets of higher profitability, that come by avoiding risk losses.” This opinion could be supported by studies by Sharma and Kumar (2011) and Abuzayed (2012) showing a positive relationship between an increasing cash conversion cycle (CCC) and increased profitability, since the increase in the CCC means moves to moderate and conservative policies.

5. Conclusion

The results of the conversations support the literature review of the article. There is consistency between what the participants contributed and the previous studies interpreted. This consistency provides results that the relation between accounting and finance is vital. It can be described as a complementary relationship.

The financial manager starts as an accountant. By getting experience, he can make critical accounting decisions. When he gains corporate finance knowledge and skill, he starts providing financial management decisions. Ultimately, by the continuous improvement in finance management and the experience, he achieves the position of the chief financial manager.

On the other hand, the relationship between working capital management and profitability is similar to the relationship between finance and accounting in many aspects. For example, the accountant needs to be familiar with financial models which provide practical methods to handle working capital elements like cash and inventory.

Additionally, many strategies can help them to manage the accounts receivable to avoid more interest that arises from the cash matching and to decrease the bad debt expense. All of the methods mentioned contribute to avoiding expenses to gain the maximum profit.

The working capital investment and financing policies have the most significant impact on profitability. These policies are related to risk and return theory since the conservative policy reduces both the risk and return and the aggressive one has the opposite impact.

The article recommends accountants to be in professional stage and increase the profitability of the company to grab both accounting and finance information and skills.

Despite the positive interview aspect, the challenges that were encountered with the meeting comprised the severe limitation of the study. When setting up the meetings with the participants, most of the sample apologised in the first attempt, and later many efforts the acceptance to conduct the meeting has been awarded. This situation has complicated the research timetable and forced the researcher to extend the research time plan to keep the methodology flow. Some meetings were time-restricted. Therefore, gaining information to suggest other research paths was not in a perfect manner.

However, the author suggests some topics for future research, for example, conducting research to provide more models to manage the working capital elements. Moreover, measuring the consequences of linking accounting with strategic management, governance and control management in education and practical experience should be done.

Sample (own sources)

Abuzayed , B. ( 2012 ), “ Working capital management and firms' performance in emerging markets: the case of Jordan ”, International Journal of Managerial Finance , Vol. 8 No. 2 , pp. 155 - 179 , doi: 10.1108/17439131211216620 .

Aguswahyudi , F.D. , Cokrodewo , A. and Sin , L.G. ( 2018 ), “ Analysis of the effectiveness of probabilistic economic order quantity (EOQ) method using model (q,r) in medication industry (case study: apotek griya medika malang) ”, Journal of International Conference Proceedings , Vol. 1 No. 1 , pp. 12 - 19 .

Ajanaku , E.A. and Ekundayo , O.A. ( 2017 ), “ Working capital management and organization performance: the relationship between working capital management and account receivable ”, Journal of Management and Corporate Governance , Vol. 9 No. 2 , pp. 59 - 84 .

Anwar , J. ( 2018 ), “ The effect of working capital management on profitability in manufacturing company listed in Indonesia stock exchange ”, The Accounting Journal of Binaniaga , Vol. 3 No. 1 , pp. 1 - 14 , doi: 10.33062/ajb.v3i1.173 .

Baños-Caballero , S. , García-Teruel , P.J. and Martínez-Solano , P. ( 2016 ), “ Financing of working capital requirement, financial flexibility and SME performance ”, Journal of Business Economics and Management , Vol. 17 No. 6 , pp. 1189 - 1204 .

Berry , A.J. , Faulkner , S. , Hughes , M. and Jarvis , R. ( 1993 ), “ Financial information, the banker and the small business ”, The British Accounting Review , Vol. 25 No. 2 , pp. 131 - 150 .

Braun , M. , Briones , I. and Islas , G. ( 2018 ), “ Interlocking directorates, access to credit, and business performance in Chile during early industrialization ”, Journal of Business Research , Vol. 105 , pp. 381 - 288 , doi: 10.1016/j.jbusres.2017.12.052 .

Brief , R.P. and Peasnell , K.V. ( 2013 ), Clean Surplus: A Link between Accounting and Finance , Routledge , Moscow .

Brusov , P. , Filatova , T. , Orehova , N. , Brusov , P. and Brusova , N. ( 2011 ), “ From modigliani–miller to general theory of capital cost and capital structure of the company ”, Research Journal of Economics, Business and ICT , Vol. 2 , pp. 16 - 21 .

Cakici , N. , Chatterjee , S. and Tang , Y. ( 2017 ), “ Alternative profitability measures and cross section of expected stock returns: international evidence ”, Working Paper , SSRN 2969687 , Springer , New York, NY , doi: 10.2139/ssrn.2969687 .

Chand , A. , Akram , S. , Akram , H. , Murad , A. and Kareem , L. ( 2019 ), “ The impact of working capital management on firm profitability: a comparison between seasonal and non-seasonal businesses ”, Research Journal of Finance and Accounting , Vol. 10 No. 15 , pp. 8 - 12 .

Cleary , P. and Quinn , M. ( 2016 ), “ Intellectual capital and business performance: an exploratory study of the impact of cloud-based accounting and finance infrastructure ”, Journal of Intellectual Capital , Vol. 17 No. 2 , pp. 255 - 278 .

Da Costa Moraes , M.B. , Nagano , M.S. and Sobreiro , V.A. ( 2015 ), Stochastic Cash Flow Management Models: A Literature Review Since the 1980s , Decision Models in Engineering and Management , Springer , pp. 11 - 28 , doi: 10.1007/978-3-319-11949-6_2 .

Daunfeldt , S.O. and Hartwig , F. ( 2014 ), “ What determines the use of capital budgeting methods?: evidence from Swedish listed companies ”, Journal of Finance and Economics , Vol. 2 No. 4 , pp. 101 - 112 .

De Jong , A. , Verbeek , M. and Verwijmeren , P. ( 2011 ), “ Firms' debt–equity decisions when the static tradeoff theory and the pecking order theory disagree ”, Journal of Banking and Finance , Vol. 35 No. 5 , pp. 1303 - 1314 .

De Wet , J. and Du Toit , E. ( 2007 ), “ Return on equity: a popular, but flawed measure of corporate financial performance ”, South African Journal of Business Management , Vol. 38 No. 1 , pp. 59 - 69 .

Droms , W.G. and Wright , J.O. ( 2010 ), Finance and Accounting for Nonfinancial Managers: All the Basics You Need to Know , Basic Books .

Fields , E. ( 2016 ), The Essentials of Finance and Accounting for Nonfinancial Managers , Amacom .

Gardiner , P.D. and Stewart , K. ( 2000 ), “ Revisiting the golden triangle of cost, time and quality: the role of NPV in project control, success and failure ”, International Journal of Project Management , Vol. 18 No. 4 , pp. 251 - 256 .

Gonen , L.D. , Weber , M. , Tavor , T. and Spiegel , U. ( 2016 ), “ A modified Baumol approach — optimal withdrawal and holding of cash liquid assets ”, Review of European Studies , Vol. 8 No. 2 , pp. 8 - 21 , doi: 10.5539/res.v8n2p8 .

Gonçalves , T. , Gaio , C. and Robles , F. ( 2018 ), “ The impact of working capital management on firm profitability in different economic cycles: evidence from the United Kingdom ”, Economics and Business Letters , Vol. 7 No. 2 , pp. 70 - 75 .

Grüter , R. and Wuttke , D.A. ( 2017 ), “ Option matters: valuing reverse factoring ”, International Journal of Production Research , Vol. 55 No. 22 , pp. 6608 - 6623 .

Hung , J.H. and Liu , Y.C. ( 2005 ), “ An empirical comparison of the capitalized cost and equivalent annual cost methods for evaluating mutually exclusive projects ”, International Journal of Management , Vol. 22 No. 2 , pp. 242 - 248 .

Jawad , H. , Jaber , M.Y. and Bonney , M. ( 2015 ), “ The economic order quantity model revisited: an extended exergy accounting approach ”, Journal of Cleaner Production , Vol. 105 , pp. 64 - 73 .

Kiyama , J.M. and Rios-Aguilar , C. ( 2017 ), “ The future of funds of knowledge in higher education ”, Funds of Knowledge in Higher Education: Honoring Students' Cultural Experiences and Resources as Strengths , Routledge , p. 68 .

Krumrey , L. , Moeini , M. and Wendt , O. ( 2017 ), “ A cash-flow-based optimization model for corporate cash management: a Monte-Carlo simulation approach ”, International Conference on Computer Science, Applied Mathematics and Applications , Springer , pp. 34 - 46 , doi: 10.1007/978-3-319-61911-8_4 .

Kwenda , F. and Holden , M. ( 2014 ), “ Determinants of working capital investment in South Africa: evidence from selected JSE-listed firms ”, Journal of Economics and Behavioral Studies , Vol. 6 No. 7 , pp. 569 - 580 .

Lazaridis , I. and Tryfonidis , D. ( 2006 ), “ Relationship between working capital management and profitability of listed companies in the Athens stock exchange ”, Journal of Financial Management and Analysis , Vol. 19 No. 1 , pp. 26 - 35 .

Mohamad , N.E.A.B. and Saad , N.B.M. ( 2010 ), “ Working capital management: the effect of market valuation and profitability in Malaysia ”, International Journal of Business and Management , Vol. 5 No. 11 , p. 140 .

Muhammad , H. , Rehman , A.U. and Waqas , M. ( 2016 ), “ The relationship between working capital management and profitability: a case study of tobacco industry of Pakistan ”, The Journal of Asian Finance, Economics and Business (JAFEB) , Vol. 3 No. 2 , pp. 13 - 20 .

Nahum-Shani , I. , Smith , S.N. , Spring , B.J. , Collins , L.M. , Witkiewitz , K. , Tewari , A. and Murphy , S.A. ( 2017 ), “ Just-in-time adaptive interventions (JITAIs) in mobile health: key components and design principles for ongoing health behavior support ”, Annals of Behavioral Medicine , Vol. 52 No. 6 , pp. 446 - 462 .

Padachi , K. ( 2006 ), “ Trends in working capital management and its impact on firms' performance: an analysis of mauritian small manufacturing firms ”, International Review of Business Research Papers , Vol. 2 No. 2 , pp. 45 - 58 .

Pais , M.A. and Gama , P.M. ( 2015 ), “ Working capital management and SMEs profitability: Portuguese evidence ”, International Journal of Managerial Finance , Vol. 11 No. 3 , pp. 341 - 358 .

Richard , E. and Kabala , B. ( 2019 ), “ Account receivable management practices of SMEs in Tanzania: a qualitative approach ”, Business and Management Review , Vol. 22 No. 2 , pp. 51 - 66 .

Righetto , G.M. , Morabito , R. and Alem , D. ( 2016 ), “ A robust optimization approach for cash flow management in stationery companies ”, Computers and Industrial Engineering , Vol. 99 , pp. 137 - 152 , doi: 10.1016/j.cie.2016.07.010 .

Sanstad , A.H. and Howarth , R.B. ( 1994 ), “ ‘Normal’ markets, market imperfections and energy efficiency ”, Energy Policy , Vol. 22 No. 10 , pp. 811 - 818 , doi: 10.1016/0301-4215(94)90139-2 .

Sharma , A.K. and Kumar , S. ( 2011 ), “ Effect of working capital management on firm profitability: empirical evidence from India ”, Global Business Review , Vol. 12 No. 1 , pp. 159 - 173 , doi: 10.1177/097215091001200110 .

Singh , H.P. , Kumar , S. and Colombage , S. ( 2017 ), “ Working capital management and firm profitability: a meta-analysis ”, Qualitative Research in Financial Markets , Vol. 9 No. 1 , pp. 34 - 47 , doi: 10.1108/QRFM-06-2016-0018 .

Van der Vliet , K. , Reindorp , M.J. and Fransoo , J.C. ( 2015 ), “ The price of reverse factoring: financing rates vs. payment delays ”, European Journal of Operational Research , Vol. 242 No. 3 , pp. 842 - 853 , doi: 10.1016/j.ejor.2014.10.052 .

Vintilă , G. and Nenu , E.A. ( 2016 ), “ Liquidity and profitability analysis on the Romanian listed companies ”, Journal of Eastern Europe Research in Business and Economics , Vol. 2016 , Art. ID , 161707 , doi: 10.5171/2016.161707 .

Wang , Z. , Xu , G. , Zhao , P. and Lu , Z. ( 2016 ), “ The optimal cash holding models for stochastic cash management of continuous time ”, Journal of Industrial and Management Optimization , Vol. 14 No. 1 , pp. 1 - 17 , doi: 10.3934/jimo.2017034 .

Wasiuzzaman , S. and Arumugam , V.C. ( 2013 ), “ Determinants of working capital investment: a study of Malaysian public listed firms ”, Australasian Accounting, Business and Finance Journal , Vol. 7 No. 2 , pp. 63 - 83 .

Zhang , G.M. and Bao , Y. ( 2018 ), Decision Analysis of Conditional Risk Method Based on Accounts Receivable Financing Mode , CCNT 2018 DEStech Publications , pp. 632 - 636 , doi: 10.12783/dtcse/CCNT2018/24769 .

Further reading

Bolton , P. and Freixas , X. ( 2000 ), “ Equity, bonds, and bank debt: capital structure and financial market equilibrium under asymmetric information ”, Journal of Political Economy , Vol. 108 No. 2 , pp. 324 - 351 .

Goncharov , I. , Mahlich , J. and Yurtoglu , B.B. ( 2018 ), “ Accounting profitability and the political process: the case of R&D accounting in the pharmaceutical industry ”, Working Paper, AF2014/15WP05 , Lancaster University Management School , SSRN 2531467 , doi: 10.2139/ssrn.2531467 .

Grundy , B.D. and Verwijmeren , P. ( 2016 ), “ Disappearing call delay and dividend‐protected convertible bonds ”, The Journal of Finance , Vol. 71 No. 1 , pp. 195 - 224 .

Martynova , N. and Perotti , E. ( 2018 ), “ Convertible bonds and bank risk-taking ”, Journal of Financial Intermediation , Vol. 35 Part B , pp. 61 - 80 , doi: 10.1016/j.jfi.2018.01.002 .

Moldovan , P.C. , Van den Broeck , T. , Sylvester , R. , Marconi , L. , Bellmunt , J. , Van den Bergh , R.C. , Bolla , M. , et al. ( 2017 ), “ What is the negative predictive value of multiparametric magnetic resonance imaging in excluding prostate cancer at biopsy? A systematic review and meta-analysis from the European association of urology prostate cancer guidelines panel ”, European Urology , Vol. 72 No. 2 , pp. 250 - 266 , doi: 10.1016/j.eururo.2017.02.026 .

Corresponding author

Related articles, we’re listening — tell us what you think, something didn’t work….

Report bugs here

All feedback is valuable

Please share your general feedback

Join us on our journey

Platform update page.

Visit emeraldpublishing.com/platformupdate to discover the latest news and updates

Questions & More Information

Answers to the most commonly asked questions here

The various domains to be covered for my essay writing.

If you are looking for reliable and dedicated writing service professionals to write for you, who will increase the value of the entire draft, then you are at the right place. The writers of PenMyPaper have got a vast knowledge about various academic domains along with years of work experience in the field of academic writing. Thus, be it any kind of write-up, with multiple requirements to write with, the essay writer for me is sure to go beyond your expectations. Some most explored domains by them are:

- Project management

Emery Evans

How Our Paper Writing Service Is Used

We stand for academic honesty and obey all institutional laws. Therefore EssayService strongly advises its clients to use the provided work as a study aid, as a source of ideas and information, or for citations. Work provided by us is NOT supposed to be submitted OR forwarded as a final work. It is meant to be used for research purposes, drafts, or as extra study materials.

Testimonials

Customer Reviews

How does this work

1035 Natoma Street, San Francisco

This exquisite Edwardian single-family house has a 1344 Sqft main…

IMAGES

VIDEO

COMMENTS

WC is the current or short-term net assets of a firm resulting from short term assets (such as cash, bank balance, receivables, closing, marketable securities, etc.) mi nus short term liabilities ...